Valid Promissory Note Document for New York

Valid Promissory Note Document for New York

When navigating the world of personal and business finance, the New York Promissory Note form emerges as a crucial document, serving as a written promise to repay borrowed money. This form not only outlines the amount borrowed but also specifies the interest rate, repayment schedule, and any applicable fees, ensuring that both the lender and borrower have a clear understanding of their obligations. In New York, the legal framework surrounding promissory notes is designed to protect both parties, making it essential to include specific details such as the maturity date and the consequences of default. Furthermore, this document can be tailored to suit various lending situations, whether for personal loans between friends or formal agreements between businesses. The simplicity and versatility of the promissory note make it a valuable tool in financial transactions, fostering trust and accountability. By understanding the components and implications of this form, individuals can better navigate their financial commitments and avoid potential disputes.

New York Promissory Note

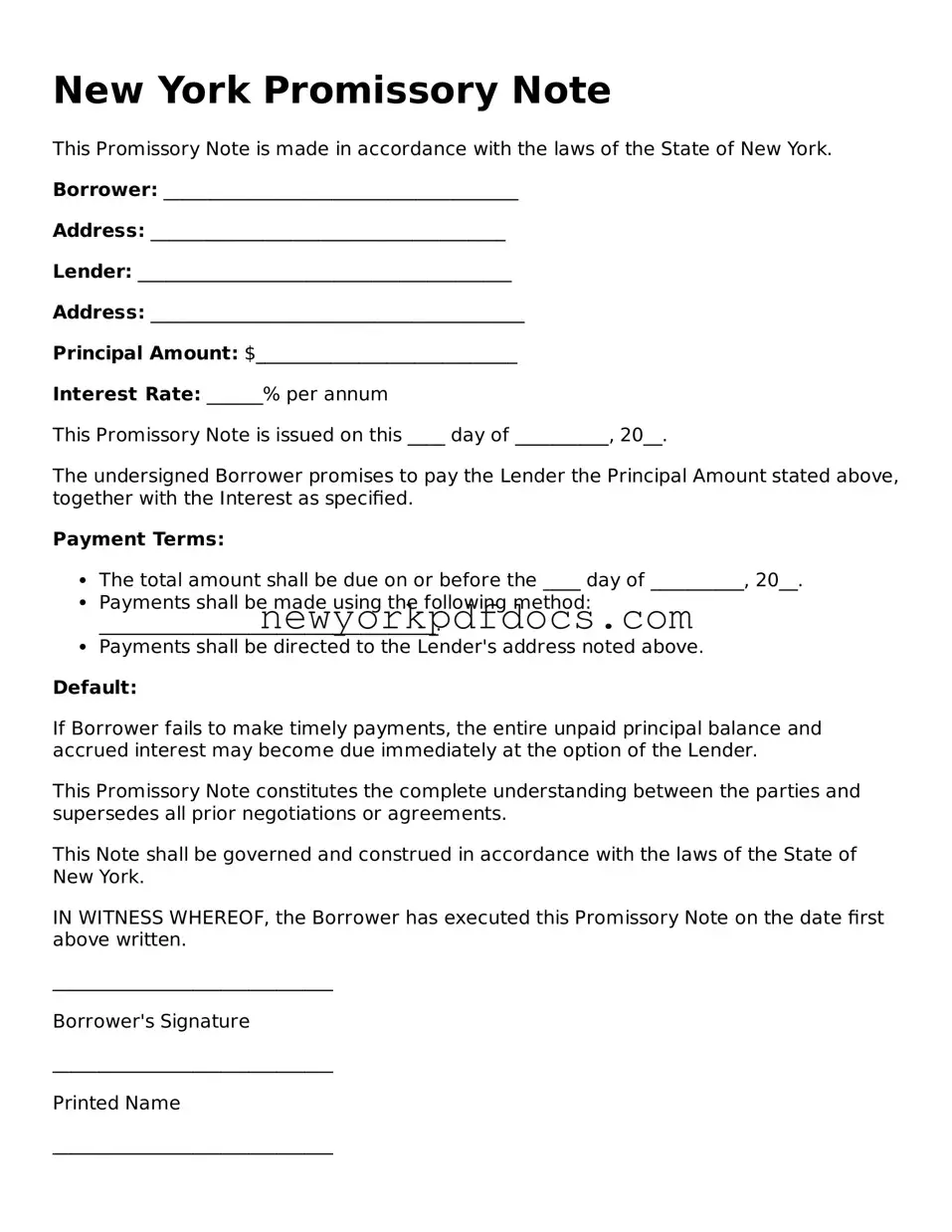

This Promissory Note is made in accordance with the laws of the State of New York.

Borrower: ______________________________________

Address: ______________________________________

Lender: ________________________________________

Address: ________________________________________

Principal Amount: $____________________________

Interest Rate: ______% per annum

This Promissory Note is issued on this ____ day of __________, 20__.

The undersigned Borrower promises to pay the Lender the Principal Amount stated above, together with the Interest as specified.

Payment Terms:

Default:

If Borrower fails to make timely payments, the entire unpaid principal balance and accrued interest may become due immediately at the option of the Lender.

This Promissory Note constitutes the complete understanding between the parties and supersedes all prior negotiations or agreements.

This Note shall be governed and construed in accordance with the laws of the State of New York.

IN WITNESS WHEREOF, the Borrower has executed this Promissory Note on the date first above written.

______________________________

Borrower's Signature

______________________________

Printed Name

______________________________

Lender's Signature

______________________________

Printed Name

When filling out the New York Promissory Note form, many individuals overlook crucial details that can lead to complications later. One common mistake is failing to include the correct names of the borrower and lender. It is essential that these names match the legal names of the parties involved. Any discrepancies can create confusion and may invalidate the document.

Another frequent error is neglecting to specify the loan amount clearly. Writing the amount in words and numbers is vital. If there is a difference between the two, it could lead to disputes. Ensuring accuracy in this section is critical for both parties to understand their obligations.

People often forget to indicate the interest rate on the loan. This detail is necessary to clarify how much the borrower will pay back over time. Without it, the agreement may lack enforceability, and misunderstandings about repayment can arise.

Additionally, many individuals do not include a repayment schedule. It is important to outline when payments are due and the method of payment. A clear timeline helps both parties stay accountable and prevents potential conflicts regarding payment expectations.

Some individuals mistakenly assume that a signature is not necessary. However, both the borrower and lender must sign the document for it to be legally binding. Without signatures, the note may not hold up in court if disputes arise.

Another oversight involves not dating the document. A date is crucial as it establishes when the agreement takes effect. This can affect the calculation of interest and the timeline for repayment.

People sometimes fail to include provisions for default. It is wise to outline what happens if the borrower fails to make payments. Including these terms can provide clarity and protect the lender’s interests.

Many overlook the need for witnesses or notarization. Depending on the circumstances, having a witness or notary public can add an extra layer of legitimacy to the document. This can be especially important if disputes occur later.

Lastly, individuals may not keep copies of the signed Promissory Note. It is essential for both parties to retain a copy for their records. This ensures that both have access to the terms of the agreement and can refer back to it as needed.

A New York Promissory Note is a written agreement in which one party promises to pay a specific amount of money to another party at a designated time or on demand. It serves as a legal document that outlines the terms of the loan or debt.

Any individual or business can use a Promissory Note. It is commonly used in personal loans, business loans, and real estate transactions. Both lenders and borrowers can benefit from having a clear, written agreement.

A typical Promissory Note includes:

Yes, a Promissory Note is a legally binding document. Once signed, both parties are obligated to adhere to the terms outlined in the note. If either party fails to comply, the other party may seek legal recourse.

No, it is not necessary to have a lawyer to create a Promissory Note. However, consulting with a legal professional can help ensure that the document meets all legal requirements and adequately protects your interests.

Yes, a Promissory Note can be modified if both parties agree to the changes. It is advisable to document any modifications in writing and have both parties sign the amended note.

If the borrower defaults, the lender may take legal action to recover the owed amount. This can include filing a lawsuit or seeking a judgment against the borrower. The specific actions depend on the terms outlined in the Promissory Note.

While there is no strict format, it is important for the note to include all essential information clearly. Using a standard template can help ensure that all necessary details are included.

It is important to keep the Promissory Note in a safe place. Both the borrower and lender should retain a signed copy for their records. This will help in case any disputes arise in the future.

Understanding the New York Promissory Note form is essential for anyone involved in lending or borrowing money. However, several misconceptions can lead to confusion. Here are ten common misconceptions, along with clarifications.

Recognizing these misconceptions can help individuals navigate the complexities of promissory notes more effectively.

Difference Between Acknowledgement and Jurat - A notary acknowledgment is a preventive measure against identity theft.

Application Rental - Explain your reason for needing a rental property at this time.

New York Premarital Contract - This form facilitates open communication about finances between partners prior to marriage.

When filling out and using the New York Promissory Note form, there are several important points to keep in mind. Here are key takeaways to consider:

Understanding these key points can help in creating a clear and enforceable Promissory Note in New York. It’s always a good idea to review the document carefully before signing.

Once you have the New York Promissory Note form in hand, it's important to ensure that all the required information is filled out accurately. Completing this form correctly is essential for establishing clear terms between the borrower and lender. Follow the steps below to guide you through the process.

With the form filled out and signed, both parties should keep their copies in a safe place. This document will serve as a record of the agreement and can be referred to in the future if any questions or issues arise.