Free Nys It 255 Form

Free Nys It 255 Form

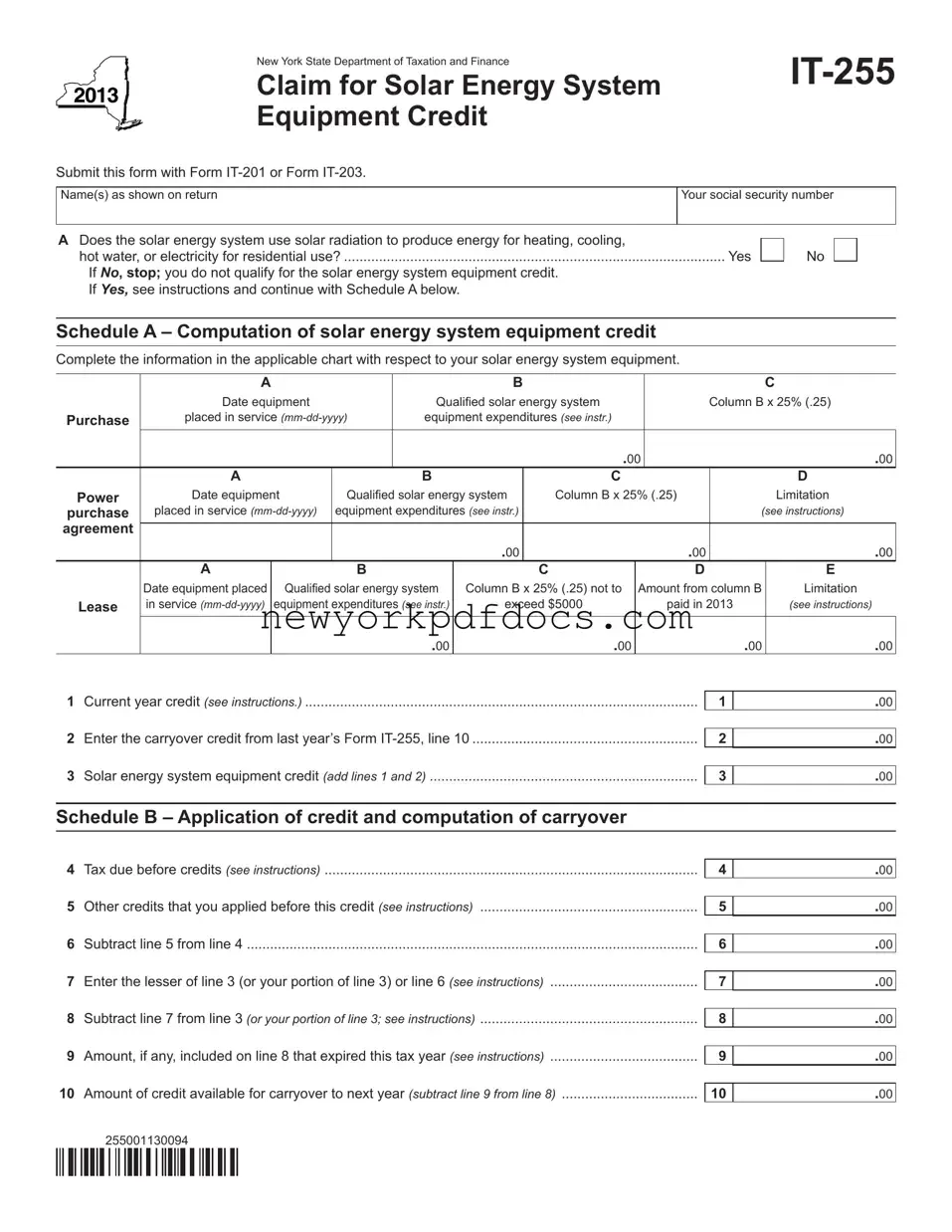

The NYS IT-255 form, officially known as the Claim for Solar Energy System Equipment Credit, is an important tool for New York taxpayers who have invested in solar energy systems. Designed by the New York State Department of Taxation and Finance, this form allows eligible residents to claim a credit for the purchase of solar energy equipment that generates energy for residential use, including heating, cooling, hot water, or electricity. To begin the process, taxpayers must submit the IT-255 alongside their income tax returns, either Form IT-201 or Form IT-203. The form includes several sections, such as Schedule A, where users calculate their credit based on qualified expenditures for solar equipment. Additionally, Schedule B helps determine how much of the credit can be applied against tax liabilities and what can be carried over to the next tax year. It’s essential for applicants to ensure that their solar energy systems meet specific criteria, as only those that utilize solar radiation for residential energy production qualify for the credit. Understanding the nuances of this form can lead to significant savings for homeowners who are making environmentally friendly choices.

New York State Department of Taxation and Finance

Claim for Solar Energy System Equipment Credit

Submit this form with Form

Name(s) as shown on return

Your social security number

ADoes the solar energy system use solar radiation to produce energy for heating, cooling,

hot water, or electricity for residential use? |

Yes |

If NO, stop; you do not qualify for the solar energy system equipment credit. |

|

If YES, see instructions and continue with Schedule A below. |

|

No

Schedule A – Computation of solar energy system equipment credit

Complete the information in the applicable chart with respect to your solar energy system equipment.

|

A |

|

|

|

B |

|

|

|

|

C |

|

Date equipment |

|

|

Qualiied solar energy system |

|

Column B x 25% (.25) |

||||

Purchase |

placed in service |

|

equipment expenditures (see instr.) |

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|

.00 |

|

A |

|

|

B |

|

C |

|

|

|

D |

Power |

Date equipment |

Qualiied solar energy system |

Column B x 25% (.25) |

|

Limitation |

|||||

purchase |

placed in service |

equipment expenditures (see instr.) |

|

|

|

(see instructions) |

||||

agreement |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

.00 |

|

.00 |

||

|

|

|

|

|

|

|

||||

|

A |

|

B |

|

C |

|

D |

E |

||

|

Date equipment placed Qualiied solar energy system |

Column B x 25% (.25) not to |

Amount from column B |

Limitation |

||||||

Lease |

in service |

exceed $5000 |

|

paid in 2013 |

(see instructions) |

|||||

|

|

|

|

|

|

|

|

|

|

|

.00

.00 |

.00 |

.00 |

1 Current year credit (see instructions.) .....................................................................................................

2 Enter the carryover credit from last year’s Form

3 Solar energy system equipment credit (add lines 1 and 2) .....................................................................

1

2

3

.00

.00

.00

Schedule B – Application of credit and computation of carryover

4 |

Tax due before credits (see instructions) |

4 |

.00 |

|

|

|

|

5 |

Other credits that you applied before this credit (see instructions) |

5 |

.00 |

|

|

|

|

6 |

Subtract line 5 from line 4 |

6 |

.00 |

|

|

|

|

7 |

Enter the lesser of line 3 (or your portion of line 3) or line 6 (see instructions) |

7 |

.00 |

|

|

|

|

8 |

Subtract line 7 from line 3 (or your portion of line 3; see instructions) |

8 |

.00 |

|

|

|

|

9 |

Amount, if any, included on line 8 that expired this tax year (see instructions) |

9 |

.00 |

|

|

|

|

10 |

Amount of credit available for carryover to next year (subtract line 9 from line 8) |

10 |

.00 |

255001130094

Filling out the NYS IT-255 form can be a straightforward process, but many people make common mistakes that can delay their tax credits. One frequent error is failing to confirm eligibility. Before proceeding, ensure that your solar energy system uses solar radiation for residential purposes such as heating, cooling, hot water, or electricity. If you answer "No" to this question, you will not qualify for the credit. Take a moment to review this requirement carefully.

Another mistake involves the computation of the solar energy system equipment credit. When completing Schedule A, it is essential to accurately fill in the date the equipment was placed in service and the corresponding expenditures. Many taxpayers mistakenly enter incorrect amounts or dates, which can lead to incorrect calculations. Remember, the credit is based on 25% of the qualified expenditures, so double-check your figures to ensure they align with the instructions.

Additionally, some individuals overlook the importance of carryover credits. If you had a carryover credit from the previous year, you must include it on line 2 of the form. Failing to do so can result in a lower credit than you are entitled to. Ensure that you have all relevant information from last year’s Form IT-255 before you submit your current form.

Lastly, be cautious when applying the credit against your tax due. On Schedule B, subtract any other credits you applied before the solar energy system equipment credit. Many people mistakenly calculate this step, which can affect the total credit available. Take your time to follow the instructions closely to avoid any miscalculations.

What is the NYS IT-255 form?

The NYS IT-255 form is a tax form used by residents of New York State to claim a credit for solar energy system equipment. This form must be submitted along with your personal income tax return, either Form IT-201 or Form IT-203.

Who is eligible to use the IT-255 form?

To qualify for the solar energy system equipment credit, your solar energy system must use solar radiation to produce energy for heating, cooling, hot water, or electricity for residential use. If your system does not meet this requirement, you will not qualify for the credit.

How do I complete Schedule A of the IT-255 form?

Schedule A requires you to provide details about your solar energy system equipment. You will need to fill in the date the equipment was placed in service, the qualified solar energy system expenditures, and calculate the credit by multiplying the expenditures by 25% (0.25). Follow the instructions carefully to ensure accurate calculations.

What is the maximum credit I can claim?

The credit is calculated based on your qualified solar energy system expenditures, but there are limitations. For certain types of agreements, the amount cannot exceed $5,000. Always refer to the instructions for specific details regarding limitations.

How do I apply the credit and calculate carryover?

In Schedule B, you will need to determine your tax due before credits and subtract any other credits you applied before the solar energy system credit. Then, you will compare the total credit available to the remaining tax due to find out how much credit can be applied this year and how much can be carried over to the next year.

What should I do if I have a carryover credit from last year?

If you have a carryover credit from the previous year, you will enter this amount on line 2 of the IT-255 form. This carryover can be added to the current year credit to determine your total solar energy system equipment credit.

What if my credit expires?

If any portion of your credit expires during the tax year, you must report this on line 9 of the IT-255 form. This amount will be subtracted from your total available credit, affecting how much you can carry over to the next year.

Where can I find more information about the IT-255 form?

For additional details, including specific instructions and guidelines, you can visit the New York State Department of Taxation and Finance website. They provide comprehensive resources to help you complete your tax forms accurately.

When is the IT-255 form due?

The IT-255 form must be submitted by the same deadline as your personal income tax return. Be sure to check the current tax year deadlines to avoid any penalties.

The New York State IT-255 form is essential for claiming the Solar Energy System Equipment Credit, but several misconceptions can lead to confusion. Here are ten common misunderstandings:

Understanding these misconceptions can help you navigate the process more effectively and ensure you take full advantage of the benefits available to you.

Vendex Nyc - Prepare to provide an explanation of any adverse actions taken against you in the past.

Nys 100 - Employers must indicate if they are registering for withholding tax exclusively on the form.

Here are key takeaways for filling out and using the NYS IT-255 form:

Completing the NYS IT-255 form is an important step for individuals who have invested in solar energy systems. This form allows you to claim a credit for the expenses related to your solar energy system equipment. Below are the steps to guide you through the process of filling out this form accurately.

After completing the form, review all entries for accuracy. Ensure that you have included any necessary supporting documents. The completed IT-255 form must be submitted alongside your Form IT-201 or Form IT-203. This submission is a crucial step in claiming your credit for the solar energy system equipment.