Free Nyc 5Ubti Form

Free Nyc 5Ubti Form

The NYC 5UBTI form is an essential document for individuals, estates, and trusts engaged in unincorporated business activities in New York City. This form allows taxpayers to declare and pay their estimated Unincorporated Business Tax (UBT) for the calendar year 2012 or their specific fiscal year. It includes sections for personal and business information, such as names, addresses, and contact details, which are crucial for accurate processing. Taxpayers must calculate their estimated tax based on their expected net income from business activities, taking into account any exemptions and applicable credits. The form also outlines payment schedules, requiring taxpayers to remit payments in installments throughout the year. If adjustments are needed, there are provisions for filing amended declarations. Timely submission is critical, as penalties may apply for late filings or underpayments. Overall, understanding and correctly completing the NYC 5UBTI form ensures compliance with local tax regulations while helping businesses manage their tax obligations effectively.

The NYC 5UBTI form is similar to several other documents used for tax purposes. Each of these documents serves a specific function, often relating to the reporting and payment of taxes for various types of entities. Below is a list of eight documents that share similarities with the NYC 5UBTI form:

Each of these forms plays a crucial role in ensuring compliance with tax obligations, just as the NYC 5UBTI does for unincorporated businesses in New York City.

|

- 5UBTI |

DECLARATION OF ESTIMATED |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2022 |

|

|||||||||

|

UNINCORPORATED BUSINESS TAX |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

(FOR INDIVIDUALS, ESTATES AND TRUSTS) |

|

||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For CALENDAR YEAR 2022 beginning ___________________________ and ending ____________________________ |

|

||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

First name and initial |

|

Last name |

Name |

n |

|

|

|

|

|

SOCIAL SECURITY NUMBER |

|

|||||||||||||||||||

Typeor |

|

|

|

|

Change |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Business name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

BUSINESS CODE NUMBER AS PER FEDERAL RETURN |

|

||||||||||||||||||||

Business address (number and street) |

|

|

|

Address |

n |

|

|

|

|||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

Change |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City and State |

|

|

Zip Code |

Country (if not US) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

ESTATES AND TRUSTS ONLY, ENTER EMPLOYER IDENTIFICATION NUMBER |

|

||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Business Telephone Number |

|

|

Taxpayer’s Email Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

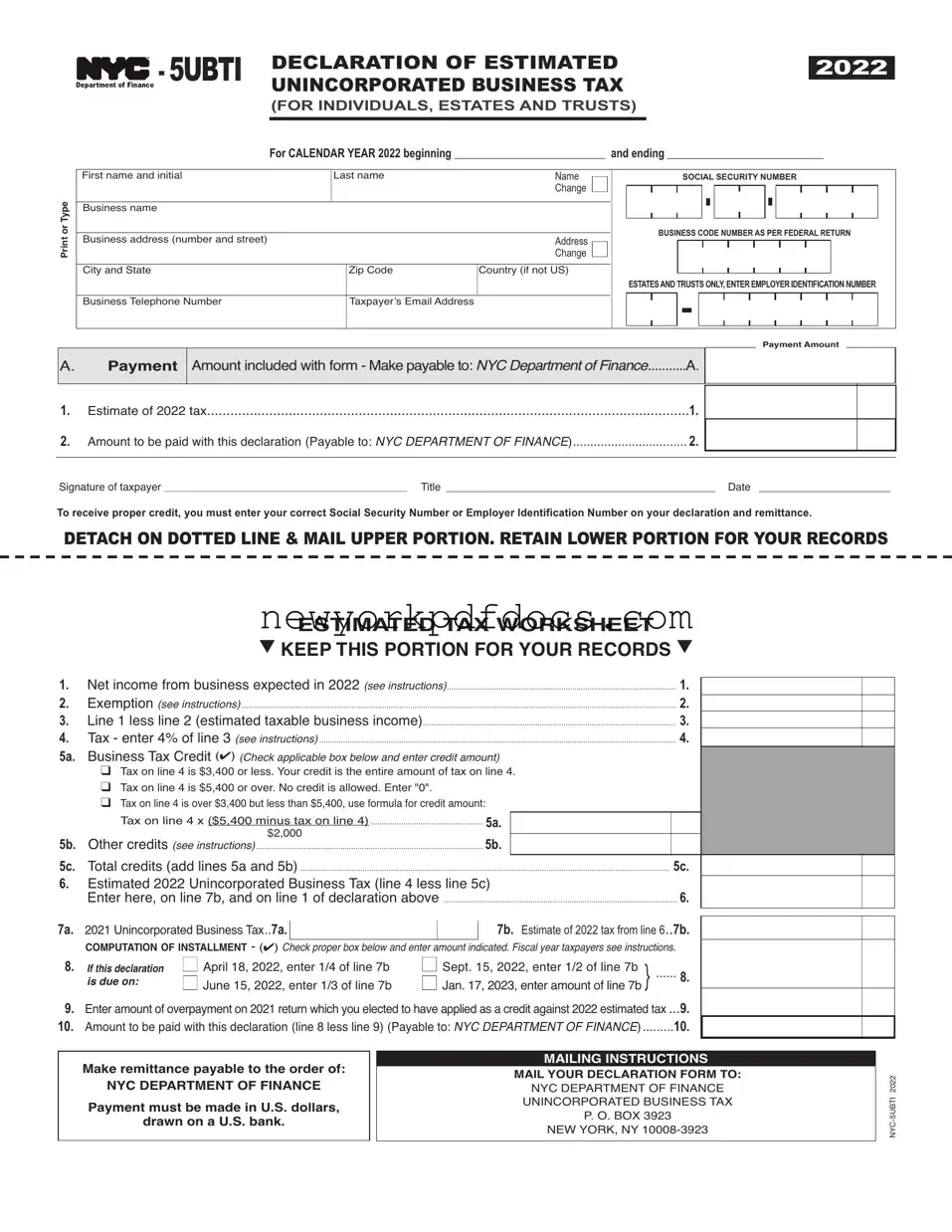

A.Payment

Amount included with form - Make payable to: NYC Department of Finance |

A. |

|

|

Payment Amount

1. |

Estimate of 2022 tax |

1. |

2. |

Amount to be paid with this declaration (Payable to: NYC DEPARTMENT OF FINANCE) |

2. |

|

|

|

Signature of taxpayer _______________________________________________________________________ Title __________________________________________________ Date ______________________

To receive proper credit, you must enter your correct Social Security Number or Employer Identification Number on your declaration and remittance.

DETACH ON DOTTED LINE & MAIL UPPER PORTION. RETAIN LOWER PORTION FOR YOUR RECORDS

|

ESTIMATED TAX WORKSHEET |

|

|

t KEEP THIS PORTION FOR YOUR RECORDS t |

|

1. |

Net income from business expected in 2022 (see instructions) |

1. |

2. |

Exemption (see instructions) |

2. |

3. |

Line 1 less line 2 (estimated taxable business income) |

3. |

4. |

Tax - enter 4% of line 3 (see instructions) |

4. |

5a. |

Business Tax Credit (4) (Check applicable box below and enter credit amount) |

|

qTax on line 4 is $3,400 or less. Your credit is the entire amount of tax on line 4.

qTax on line 4 is $5,400 or over. No credit is allowed. Enter "0".

qTax on line 4 is over $3,400 but less than $5,400, use formula for credit amount:

|

Tax on line 4 x ($5,400 minus tax on line 4) |

|

5a. |

|

|

|

|

|

|

|||||

5b. |

|

.........................................................................................................$2,000 |

|

|

|

|

5b. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

Other credits (see instructions) |

|

|

|

|

|

|

|

|

||||||

5c. |

Total credits (add lines 5a and 5b) |

|

|

|

|

5c. |

||||||||

6. |

Estimated 2022 Unincorporated Business Tax (line 4 less line 5c) |

|

|

6. |

|

|

||||||||

|

Enter here, on line 7b, and on line 1 of declaration above |

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|||||||

7a. 2021 Unincorporated Business Tax..7a. |

|

|

|

|

|

7b. Estimate of 2022 tax from line 6..7b. |

|

|

||||||

|

COMPUTATION OF INSTALLMENT - (4) Check proper box below and enter |

amount indicated. Fiscal year taxpayers see instructions. |

|

|

|

|||||||||

8. |

If this declaration |

n April 18, 2022, enter 1/4 of line 7b |

n Sept. 15, 2022, enter 1/2 of line 7b |

...... |

|

|

|

|||||||

|

is due on: |

n June 15, 2022, enter 1/3 of line 7b |

n Jan. 17, 2023, enter amount of line 7b } |

8. |

|

|

||||||||

|

|

|

|

|

||||||||||

9. Enter amount of overpayment on 2021 return which you elected to have applied as a credit against 2022 estimated tax ...9. |

|

|||||||||||||

10. |

Amount to be paid with this declaration (line 8 less line 9) (Payable to: NYC DEPARTMENT OF FINANCE) .........10. |

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|||||

|

Make remittance payable to the order of: |

|

|

|

|

|

MAILING INSTRUCTIONS |

|||||||

|

|

|

|

|

|

MAIL YOUR DECLARATION FORM TO: |

||||||||

|

NYC DEPARTMENT OF FINANCE |

|

|

|

|

|

||||||||

|

|

|

|

|

|

NYC DEPARTMENT OF FINANCE |

||||||||

|

Payment must be made in U.S. dollars, |

|

|

|

|

|

UNINCORPORATED BUSINESS TAX |

|||||||

|

|

|

|

|

|

P. O. BOX 3923 |

|

|

|

|||||

|

drawn on a U.S. bank. |

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

NEW YORK, NY |

||||||||

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Form |

Page 2 |

NOTE

If any due date falls on Saturday, Sunday or legal holiday, filing will be timely if made by the next day which is not a Saturday, Sunday or holiday.

PURPOSE OF DECLARATION

This declaration form provides a means of paying Unincorporated Business Tax on a current basis for individuals, estates and trusts engaged in carrying on an unincorporated business or profession, as defined in Section

Every unincorporated business must file an income tax return after the close of its taxable year and pay any balance of tax due. If the tax has been overpaid, adjustment will be made only after the return has been filed.

WHO MUST MAKE A DECLARATION

A 2022 declaration must be made by every individual, estate and trust carrying on an unincor- porated business or profession in New York City if its estimated tax (line 6 of tax computation schedule) can reasonably be expected to exceed $3,400 for the calendar year 2022 (or, in the case of a fiscal year taxpayer, for the fiscal year beginning in 2022).

WHEN AND WHERE TO FILE DECLARATION

You must file the declaration for the calendar year 2022 on or before April 18, 2022, or on the applicable later dates specified in these instructions.

Mail your declaration form with or without remittance to:

NYC Department of Finance

Unincorporated Business Tax

P. O. Box 3923

New York, NY

Fiscal year taxpayers, read instructions opposite regarding filing dates.

HOW TO ESTIMATE UNINCORPORATED BUSINESS TAX The worksheet on the front of this form will help you in estimating the tax for 2022.

LINE 1 -

The term “net income from business expected in 2022” means the amount estimated to be the 2022 net income from business, including professions, before the unincorporated business ex- emption. See Schedule A, line 14 of the 2021 Unincorporated Business Tax Return and related instructions (Form

LINE 2 - EXEMPTION

For the amount of the allowable exemption, see the instructions for the 2021 Form

LINE 4 - UNINCORPORATED BUSINESS TAX

If you expect to receive a refund or credit in 2022 of any sales or compensating use tax for which a credit was claimed in a prior year under Administrative Code Section

LINE 5b - OTHER CREDITS

Enter on line 5b the amount estimated to be the sum of any credits allowable for 2022 under Ad- ministrative Code Sections

Make remittance payable to NYC DEPARTMENT OF FINANCE. All remittances must be payable in U. S. dollars drawn on a U. S. bank. Checks drawn on foreign banks will be rejected and returned. A separate check for the declaration will expedite processing of the payment.

AMENDED DECLARATION

If, after a declaration is filed, the estimated tax increases or decreases because of a change in income, deductions, or allocation, you should file an amended declaration on or before the next date for payment of an installment of estimated tax.

CHARGE FOR UNDERPAYMENT OF INSTALLMENTS OF ESTIMATED TAX

A charge is imposed for underpayment of an installment of estimated tax for 2022. For infor- mation regarding interest rates, call 311. If calling from outside of the five NYC boroughs, please call

PENALTIES

The law imposes penalties for failure to make a declaration or pay estimated tax due or for making a false or fraudulent declaration or certification.

FISCAL YEAR TAXPAYERS

A taxpayer filing its Unincorporated Business Tax Return on a fiscal year basis should substi- tute the corresponding fiscal year months for the months specified in the instructions. For ex- ample, if the fiscal year begins on April 1, 2022, the Declaration of Estimated Unincorporated Business Tax will be due on July 15, 2022, together with payment of first quarter estimated tax. In this case, equal installments will be due on or before September 15, 2022, December 15, 2022, and April 18, 2023.

CHANGES IN INCOME

Even though on April 18, 2022, you do not expect your unincorporated business tax to exceed $3,400, a change in income, allocation or exemption may require that a declaration be filed later. In this event the requirements are as follows:

If requirement for filing occurs: |

File |

Amount of |

|

Installment |

|

declaration by: |

estimated |

|

payment |

||

|

|

|

tax due |

|

dates |

after |

but before |

|

|

|

|

|

|

|

|

|

|

April 1, 2022 |

June 1, 2022 |

June 15, 2022 |

1/3 |

(1) |

June 15, 2022 |

|

|

|

|

(2) |

Sept. 15, 2022 |

|

|

|

|

(3) |

Jan. 17, 2023 |

June 1, 2022 |

Sept. 1, 2022 |

Sept. 15, 2022 |

1/2 |

(1) |

Sept. 15, 2022 |

|

|

|

|

(2) |

Jan. 17, 2023 |

|

|

|

|

|

|

Sept. 1, 2022 |

Jan. 1, 2023 |

Jan. 17, 2023 |

100% |

|

None |

|

|

|

|

|

|

If you file your 2022 Unincorporated Business Tax Return by February 15, 2023, and pay the full balance of tax due, you need not: (a) file an amended declaration or an original declaration otherwise due for the first time on January 17, 2023, or (b) pay the last installment of estimated tax otherwise due and payable on January 17, 2023.

CAUTION

An extension of time to file your federal tax return or New York State personal income tax re- turn does NOT extend the filing date of your New York City tax return.

ELECTRONIC FILING

Note: Register for electronic filing. It is an easy, secure and convenient was to file a declara- tion and an extension and pay taxes

For more information log on to NYC.gov/eservices

NOTE

Filing a declaration or an amended declaration, or payment of the last installment on January 17, 2023, or filing a tax return by February 15, 2023, will not satisfy the filing requirements if you failed to file or pay an estimated tax which was due earlier in the taxable year.

PRIVACY ACT NOTIFICATION

The Federal Privacy Act of 1974, as amended, requires agencies requesting Social Security Numbers to in- form individuals from whom they seek this information as to whether compliance with the request is vol- untary or mandatory, why the request is being made and how the information will be used. The disclosure of Social Security Numbers for taxpayers is mandatory and is required by section

To receive proper credit, you must enter your correct Social Security Number or Employer Identification Number on your declaration and remittance.

Filling out the NYC 5UBTI form can be a straightforward process, but many people make common mistakes that can lead to delays or issues with their tax filings. One frequent error is failing to provide the correct Social Security Number or Employer Identification Number. This number is essential for the Department of Finance to accurately process your declaration and ensure you receive proper credit for your payments. Always double-check that you have entered this information correctly before submitting the form.

Another mistake is neglecting to calculate the estimated tax accurately. Many individuals either underestimate or overestimate their net income from business expected for the year. This can happen if someone does not take into account all sources of income or fails to apply the proper exemptions. Using the worksheet provided on the form can help in making a more accurate estimate. It’s crucial to ensure that the figures you enter reflect your actual business activities.

People also often overlook the importance of payment details. When submitting the form, ensure that you include the correct payment amount. This includes any overpayments from the previous year that you wish to apply as a credit against your current estimated tax. Missing or incorrect payment amounts can result in penalties or delays in processing. Be sure to check the payment instructions carefully and make your remittance payable to the NYC Department of Finance.

Lastly, many individuals miss the filing deadline. The declaration must be filed by April 17, 2012, or the applicable later dates specified in the instructions. If you miss this deadline, you may face penalties or interest charges. It’s important to mark your calendar and set reminders to ensure that your declaration and payment are submitted on time. Keeping track of these dates can save you from unnecessary complications.

What is the NYC 5UBTI form?

The NYC 5UBTI form is a declaration used for the Unincorporated Business Tax (UBT) in New York City. It is specifically for individuals, estates, and trusts that operate unincorporated businesses. This form allows taxpayers to estimate their tax liability for the calendar year 2012 or their fiscal year. Completing this form ensures that the business pays its taxes on time and avoids penalties.

Who needs to file the NYC 5UBTI form?

Any individual, estate, or trust that expects its Unincorporated Business Tax to exceed $3,400 for the year must file this declaration. This includes anyone engaged in carrying on an unincorporated business or profession in New York City. Partnerships, however, should use a different form, the NYC-5UB.

When is the NYC 5UBTI form due?

The form must be filed by April 17, 2012, for the calendar year 2012. If you are filing for a fiscal year, the due date will vary based on your specific fiscal year start date. If the due date falls on a weekend or holiday, you can file on the next business day without penalty.

How do I estimate my Unincorporated Business Tax?

To estimate your tax, use the worksheet provided on the NYC 5UBTI form. Start by calculating your net income from the business expected in 2012. Then, subtract any exemptions. Multiply the resulting figure by 4% to determine your estimated tax. If you have any applicable credits, subtract those from your tax calculation as well. This will give you the amount you need to report on the form.

Misconception 1: The NYC 5UBTI form is only for corporations.

This form is specifically designed for individuals, estates, and trusts that engage in unincorporated business activities. Corporations must use a different form, namely the NYC-5UB.

Misconception 2: Filing the NYC 5UBTI form is optional.

If your estimated Unincorporated Business Tax is expected to exceed $3,400 for the calendar year, filing this declaration is mandatory. Failing to do so may lead to penalties.

Misconception 3: You can file the form anytime during the year.

The declaration must be filed by April 17, 2012, or on the applicable later dates specified in the instructions. Timely filing is crucial to avoid late fees.

Misconception 4: You don’t need to pay if you filed a declaration.

Payment is required along with the declaration. You can pay in installments, but the first installment must accompany the declaration to avoid penalties.

Misconception 5: Only one payment method is accepted.

While checks are a common payment method, payments must be made in U.S. dollars and drawn on a U.S. bank. Other payment methods may be available, so it’s wise to check the latest guidelines.

Misconception 6: If I file late, I can still avoid penalties.

Late filings can incur penalties. If you miss the deadline, it’s important to file as soon as possible to mitigate potential charges for underpayment or late submission.

Nycha Careers - Supporting medical documentation is encouraged for the evaluation of requests.

Can I Get a Copy of My New York Marriage Certificate Online - It is important to follow the instructions carefully to guarantee a smooth process.

How to Fill Out Anti Arson Application - Code violations must be disclosed to help assess the property’s risk level.

When filling out and using the NYC 5UBTI form, consider the following key takeaways:

Completing the NYC 5UBTI form requires careful attention to detail. Each section must be filled out accurately to ensure proper processing. After you submit your form, the New York City Department of Finance will review your information and determine your estimated tax obligations.