Free Nyc 4S Form

Free Nyc 4S Form

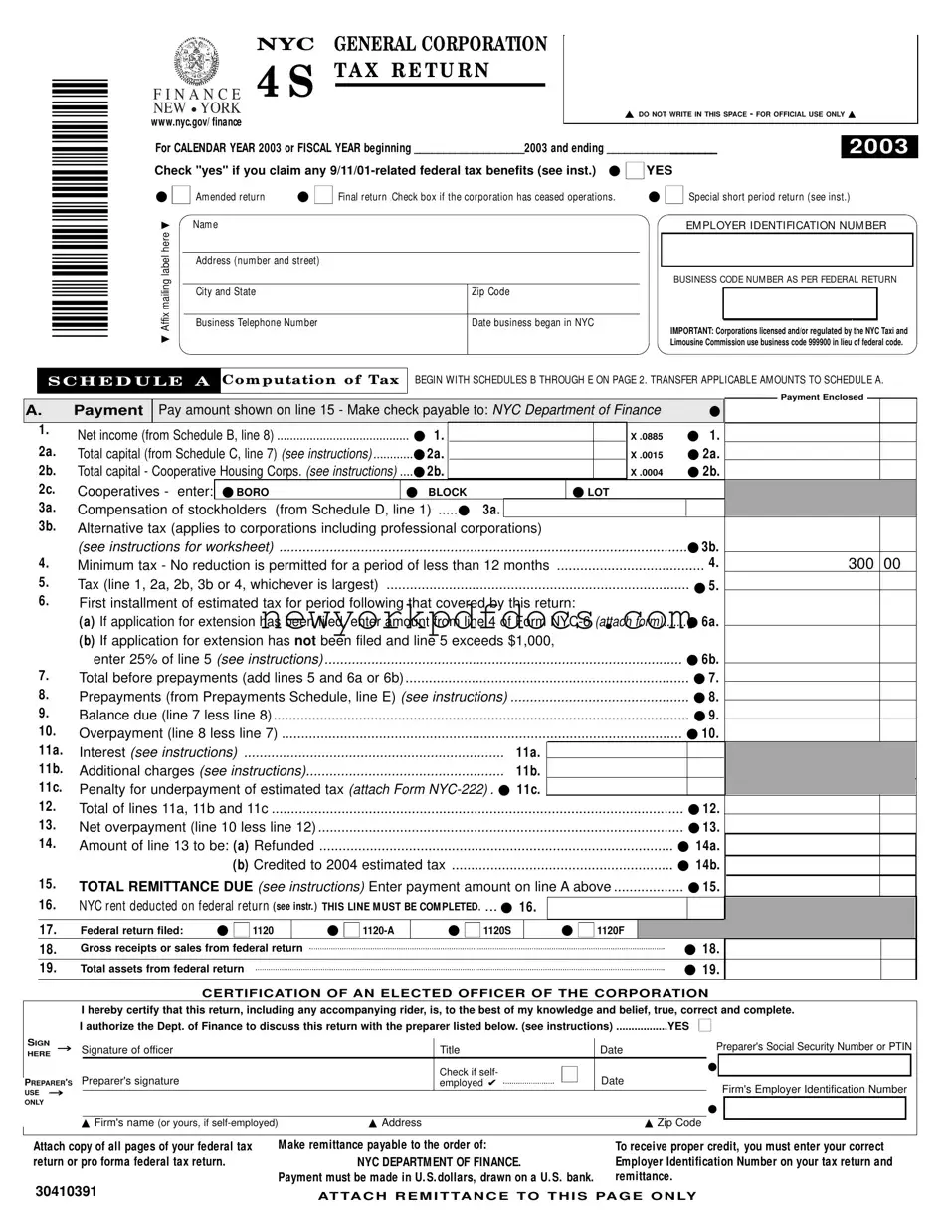

For businesses operating in New York City, the NYC 4S form plays a crucial role in tax compliance. This form is specifically designed for general corporations and is essential for reporting various financial details related to the corporation’s income, capital, and stockholder compensation. The form requires corporations to provide their Employer Identification Number (EIN), business address, and the specific business code as per their federal return. Additionally, corporations must indicate whether they are claiming any federal tax benefits related to the events of September 11, 2001, and whether this return is amended or final. The NYC 4S form also includes several schedules that guide businesses in calculating their taxable net income, total capital, and stockholder compensation. Accurate completion of these sections is vital, as it determines the tax liability owed to the city. Furthermore, the form outlines the necessary steps for making payments and claiming any overpayments, ensuring that corporations can navigate their financial obligations effectively. As the due date for filing approaches, understanding the intricacies of the NYC 4S form becomes paramount for compliance and financial planning.

*30410391*

|

NYC GENERAL CORPORATION |

|

|

|

|

|

|

|

|

|

|

||||||

F I N A N C E 4 S |

T A X R E T U R N |

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

NEW ● YORK |

|

|

|

|

|

|

|

▲ DO NOT WRITE IN THIS SPACE - FOR OFFICIAL USE ONLY ▲ |

|

||||||||

www.nyc.gov/ finance |

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

||||||||

For CALENDAR YEAR 2003 or FISCAL YEAR beginning ___________________2003 and ending ___________________ |

2003 |

|

|||||||||||||||

Check "yes" if you claim any |

|

|

|

|

|||||||||||||

● ■ Am ended return |

● ■ Final return .Check box if the corporation has ceased operations. |

|

● ■ Special short period return (see inst.) |

|

|||||||||||||

▼ |

Nam e |

|

|

|

|

|

|

|

|

|

|

EM PLOYER IDENTIFICATION NUM BER |

|

||||

here |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

label |

Address (num ber and street) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

mailing |

|

|

|

|

|

|

|

|

|

|

|

BUSINESS CODE NUM BER AS PER FEDERAL RETURN |

|

|

|||

Affix |

City and State |

|

|

|

|

Zip Code |

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Business Telephone Num ber |

|

|

|

Date business began in NYC |

|

|

|

|

|

|

|

|

|

||||

▼ |

|

|

|

|

|

|

IMPORTANT: Corporations licensed and/or regulated by the NYC Taxi and |

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

Limousine Commission use business code 999900 in lieu of federal code. |

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

S C H E D U LE A |

|

Com putation of Tax |

|

BEGIN WITH SCHEDULES B THROUGH E ON PAGE 2. TRANSFER APPLICABLE AM OUNTS TO SCHEDULE A. |

|||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Payment Enclosed |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A. |

Payment |

Pay amount shown on line 15 - Make check payable to: NYC Department of Finance |

|

● |

|

|

|

|

|

|||||||||||||||||||

|

|

|

|

|

||||||||||||||||||||||||

1. |

Net income (from Schedule B, line 8) |

|

|

|

|

● 1. |

|

|

|

|

|

|

|

|

|

X .0885 |

|

● 1. |

|

|

|

|

|

|||||

|

|

........................................ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

2a. |

Total capital (from Schedule C, line 7) (see instructions) |

● 2a. |

|

|

|

|

|

|

|

|

|

X .0015 |

|

● 2a. |

|

|

|

|

|||||||||

|

2b. |

Total capital - Cooperative Housing Corps. (see instructions) .... |

● 2b. |

|

|

|

|

|

|

|

|

|

X .0004 |

|

● 2b. |

|

|

|

|

|||||||||

|

2c. |

Cooperatives - enter: |

● BORO |

|

|

|

● BLOCK |

|

|

|

|

|

|

● LOT |

|

|

|

|

|

|

|

|||||||

|

3a. |

Compensation of stockholders |

(from Schedule D, line 1) |

● |

3a. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

3b. |

Alternative tax (applies to corporations including professional corporations) |

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

(see instructions for worksheet) |

......................................................................................................... |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

● 3b. |

|

|

|

|

||||

4. |

Minimum tax - No reduction is permitted for a period of less than 12 months |

...................................... |

|

|

|

|

4. |

|

300 |

00 |

||||||||||||||||||

5. |

Tax (line 1, 2a, 2b, 3b or 4, whichever is largest) |

|

|

|

|

|

|

|

|

|

|

|

|

|

● 5. |

|

|

|

|

|||||||||

6. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

First installment of estimated tax for period following that covered by this return: |

|

|

|

|

|

|

|

|||||||||||||||||||||

|

|

( a) If application for extension has been filed, enter amount from line 4 of Form |

....... |

● 6a. |

|

|

|

|

||||||||||||||||||||

|

|

|

|

|

|

|

||||||||||||||||||||||

|

|

( b) If application for extension has not been filed and line 5 exceeds $1,000, |

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

7. |

enter 25% of line 5 (see instructions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

● 6b. |

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

Total before prepayments (add lines 5 and 6a or 6b) |

......................................................................... |

|

|

|

|

|

|

|

|

|

|

|

|

|

● 7. |

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

8. |

Prepayments (from Prepayments Schedule, line E) (see instructions) |

|

|

|

|

|

● 8. |

|

|

|

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

||||||||||||||||||||

9. |

Balance due (line 7 less line 8) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

● 9. |

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

10. |

Overpayment (line 8 less line 7) |

|

|

|

|

|

|

|

|

|

|

|

|

|

● 10. |

|

|

|

|

|||||||||

|

11a. |

...................................................................Interest (see instructions) |

|

|

|

|

|

|

11a. |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

11b. |

...................................................Additional charges (see instructions) |

|

|

|

11b. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

11c. |

Penalty for underpayment of estimated tax (attach Form |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

12. |

Total of lines 11a, 11b and 11c |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

● 12. |

|

|

|

|

|

|||||

13. |

Net overpayment (line 10 less line 12) |

|

|

|

|

|

|

|

|

|

|

|

|

|

● 13. |

|

|

|

|

|||||||||

14. |

...........................................................................................Amount of line 13 to be: ( a) Refunded |

|

|

|

|

|

|

|

|

|

|

|

|

● 14a. |

|

|

|

|

||||||||||

|

|

|

|

|

( b) Credited to 2004 estimated tax |

......................................................... |

|

|

|

|

|

|

|

|

|

● 14b. |

|

|

|

|

||||||||

15. |

..................TOTAL REMITTANCE DUE (see instructions) Enter payment amount on line A above |

● 15. |

|

|

|

|

||||||||||||||||||||||

16. |

NYC rent deducted on federal return (see instr. ) THIS LINE M UST BE COM PLETED. |

... ● 16. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

17. |

Federal return filed: |

● ■ 1120 |

|

● ■ |

|

|

● ■ 1120S |

|

|

|

● ■ 1120F |

|

|

|

|

|

|

|

|

||||||||

|

18. |

Gross receipts or sales from federal return |

|

|

|

|

|

|

|

|

|

|

|

|

|

● 18. |

|

|

|

|

|

|||||||

|

19. |

Total assets from federal return |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

● 19. |

|

|

|

|

|

||||

CERTIFICATION OF AN ELECTED OFFICER OF THE CORPORATION

SIGN →

HERE

PREPARER'S USE →

ONLY

I hereby certify that this return, including any accompanying rider, is, to the best of my knowledge and belief, true, correct and complete.

I authorize the Dept. of Finance to discuss this return with the preparer listed below. (see instructions) .................YES ■ |

|

|

|

||||||

Signature of officer |

|

Title |

|

Date |

Preparer's Social Security Number or PTIN |

||||

|

|

||||||||

|

|

|

Check if self- |

■ |

|

● |

|

|

|

Preparer's signature |

|

Date |

|

|

|

||||

|

employed ✔ |

Firm's Employer Identification Number |

|||||||

|

|

|

|

|

|

● |

|||

|

|

|

|

|

|

|

|

|

|

▲ Firm's name (or yours, if |

▲ Address |

|

▲ Zip Code |

|

|

|

|||

|

|

|

|

||||||

Attach copy of all pages of your federal tax |

M ake remittance payable to the order of: |

return or pro forma federal tax return. |

NYC DEPARTM ENT OF FINANCE. |

|

Payment must be made in U. S. dollars, drawn on a U. S. bank. |

To receive proper credit, you must enter your correct Employer Identification Number on your tax return and remittance.

30410391 |

AT TA C H R E M I T TA N C E T O T H I S PA G E O N LY |

|

Form |

NAME _____________________________________________________________ EIN __________________________ |

Page 2 |

||||||||

|

|

|

|

|

|

|

||||

S C H E D U LE B |

Com putation of N YC Taxable N et Incom e |

|

|

|

|

|

||||

|

|

|

|

|

1. |

|

|

|

||

1. |

Federal taxable income before net operating loss deduction and special deductions (see instructions) .. |

|

|

|

||||||

2. |

.................................Interest on federal, state, municipal and other obligations not included in line 1 |

|

|

|

||||||

|

|

|

||||||||

3a. |

NYS Franchise Tax and other income taxes, including MTA surcharge, deducted on federal return (see instr.) |

3a. |

|

|

|

|||||

|

|

|

||||||||

3b. |

NYC General Corporation Tax deducted on federal return (see instructions) |

3b. |

|

|

|

|||||

|

|

|

||||||||

4. |

ACRS depreciation and/or adjustment (attach Form |

4. |

|

|

|

|||||

|

|

|

||||||||

5. |

Total (sum of lines 1 through 4) |

|

|

5. |

|

|

|

|||

6a. |

..........New York City net operating loss deduction (see instructions) |

6a. |

|

|

|

|

|

|

||

6b. |

Depreciation and/or adjustment calculated under |

|

|

|

|

S CORPORATIONS |

||||

|

|

|

|

|||||||

|

pre - 9/11/01 rules (attach Form |

6b. |

|

|

|

see instructions |

||||

6c. |

NYC and NYS tax refunds included in Schedule B, |

|

|

|

|

for line 1 |

||||

|

|

|

|

|

|

|

||||

|

line 1 (see instructions) |

6c. |

|

|

|

|

|

|

||

7. |

.........................................................................................................Total (sum of lines 6a through 6c) |

|

|

7. |

|

|

|

|||

|

|

|

|

|

|

|||||

8. |

Taxable net income (line 5 less line 7) (enter on page 1, Schedule A, line 1) (see instructions) |

8. |

|

|

|

|||||

S C H E D U LE C

Total Capital

Basis used to determine average value in column C. CHECK ONE. (ATTACH DETAILED SCHEDULE)

■ - Annually |

■ - |

■ - Quarterly |

|

COLUMN A |

|

COLUMN B |

|

COLUMN C |

|||||

|

|

|

|

|

|

Beginning of Year |

|

End of Year |

|

Average Value |

|||

■ |

- Monthly |

■ - Weekly |

■ - Daily |

||||||||||

|

|

|

|

|

|

|

|

||||||

1. |

Total assets from federal return |

1. |

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|||||||

2. |

Real property and marketable securities included in line 1 |

2. |

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|||||||

3. |

Subtract line 2 from line 1 |

3. |

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|||||||

4. |

Real property and marketable securities at fair market value |

4. |

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|||||||

5. |

Adjusted total assets (add lines 3 and 4) |

5. |

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|||||||

6. |

Total liabilities (see instructions) |

6. |

|

|

|

|

|

|

|

||||

7. |

Total capital (column C, line 5 less column C, line 6) (enter on page 1, Schedule A, line 2a or 2b) |

.......................... |

7. |

|

|

||||||||

|

|

|

|||||||||||

S C H E D U LE D

Cer tain Stockhold ers

Include all stockholders owning in excess of 5% of taxpayer's issued capital stock who received any compensation, including commissions.

Name and Address - Give actual residence (Attach rider if necessary)

Social Security Number

Official Title

Salary & All Other Compensation

Received from Corporation

(If none, enter "0")

1. Total, including any amount on rider (enter on page 1, Schedule A, line 3a) |

1. |

S C H E D U LE E

The following infor m ation m us t be entered for this retur n to be com plete .

1.

2.

3.

*30420391*

New York City principal business activity |

|

|

|

|

|

||

|

|

|

|

|

|

|

|

Does the corporation have an interest in real property located in New York City? (see instructions) |

YES |

■ |

NO |

■ |

|||

If "YES": (a) |

Attach a schedule of such property, including street address, borough, block and lot number. |

|

■ |

|

■ |

||

(b) Was a controlling economic interest in this corporation (i.e., 50% or more of stock ownership) transferred during the tax year?.... |

YES |

NO |

|||||

4. |

Does the corporation have one or more qualified subchapter s subsidiaries (QSSS)? |

YES |

■ |

NO |

■ |

||

If "YES" Attach a schedule showing the name, address and EIN, if any, of each QSSS and indicate whether the QSSS filed or was required to file a City business income tax return. See instructions.

|

PREPAYMENTS CLAIMED ON SCHEDULE A, LINE 8 |

|

DATE |

|

AMOUNT |

|

TWELVE DIGIT TRANSACTION ID CODE |

|||

|

....A. Mandatory first installment paid with preceding year's tax |

|

|

|

|

|

|

|

|

|

|

.............Payment with declaration, Form |

|

|

|

|

|

|

|

|

|

|

B. Payment with Notice of Estimated Tax Due, (2) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

Payment with Estimated Tax Due (3) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

C.Payment with extension, Form |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

D.Overpayment credited from preceding year |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

E. TOTAL of A, B, C and D (enter on Schedule A, line 8) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

M A I L I N G |

RETURNS WITH REMITTANCES |

RETURNS CLAIMING REFUNDS |

ALL OTHER RETURNS |

2003 |

|||||

|

NYC DEPARTMENT OF FINANCE |

NYC DEPARTMENT OF FINANCE |

NYC DEPARTMENT OF FINANCE |

|||||||

|

INSTRUCTIONS |

PO BOX 5040 |

PO BOX 5050 |

|

|

|

|

- |

||

|

|

PO BOX 5060 |

||||||||

|

|

KINGSTON, NY |

KINGSTON, NY |

KINGSTON, NY |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

30420391 The due date for the calendar year 2003 return is on or before March 15, 2004. For fiscal years beginning in 2003, File within 2 1/2 months after the close of fiscal year. |

|||||||||

|

|

|||||||||

Filling out the NYC 4S form can be a straightforward process, but many people stumble due to common mistakes. One frequent error is neglecting to check the correct boxes. For instance, if a corporation has ceased operations, it’s essential to mark the appropriate box indicating a final return. Failing to do so can lead to confusion and potential delays in processing.

Another mistake involves the Employer Identification Number (EIN). It’s crucial to enter the correct EIN on the form. An incorrect number can result in the return being misfiled or rejected. Always double-check this information before submitting the form.

Many individuals also overlook the importance of including all required schedules. The NYC 4S form references several schedules that must be completed and attached. If these are missing, the form may be deemed incomplete, leading to further complications down the line.

Additionally, some people forget to sign the form. The certification by an elected officer of the corporation is mandatory. Without this signature, the return may not be considered valid, which could result in penalties or other issues.

Another common error is miscalculating the tax amounts. Whether it’s the net income, capital, or any other figures, double-checking calculations can save time and prevent errors. Simple arithmetic mistakes can lead to significant discrepancies in tax owed.

People often fail to provide adequate information about stockholders. The form requires details about stockholders owning more than 5% of the issued capital stock. Omitting this information can lead to incomplete filings and possible audits.

Many also neglect to attach the necessary federal tax return copies. The instructions specify that all pages of the federal return or pro forma return must be attached. Failing to include these documents can result in delays in processing.

Another mistake is not reviewing the mailing instructions. Each type of return has a specific mailing address. Sending the return to the wrong address can cause significant delays in processing and could even result in penalties.

Finally, many people miss the deadline for filing. The due date for the 2003 return is March 15, 2004. Failing to file on time can lead to penalties and interest charges, so it’s important to mark your calendar and plan ahead.

The NYC 4S form is a tax return specifically for corporations operating in New York City. It is used to report the corporation's income, capital, and other relevant financial information for the tax year. This form is essential for calculating the amount of tax owed to the city.

Any corporation that conducts business in New York City and meets certain income thresholds is required to file the NYC 4S form. This includes general corporations, cooperatives, and professional corporations. If your corporation has ceased operations, you must indicate this on the form.

The due date for the NYC 4S form for the calendar year 2003 is March 15, 2004. For corporations operating on a fiscal year, the return must be filed within 2.5 months after the end of the fiscal year. Timely filing is crucial to avoid penalties.

The form requires various details, including the corporation's name, Employer Identification Number (EIN), business address, and the dates of operation. Additionally, corporations must provide financial information such as net income, total capital, and compensation of stockholders. Accurate reporting is essential to ensure compliance.

The tax is calculated based on several factors, including net income and total capital. The form outlines specific tax rates, such as 0.0885% on net income and 0.0015% on total capital. Corporations must determine which of these calculations results in the highest tax liability and report that amount.

If a corporation overpays its taxes, it can claim a refund or apply the overpayment to the next year's estimated tax. The form includes sections to indicate how to handle any overpayment. It is important to follow the instructions carefully to ensure the correct processing of refunds or credits.

Failing to file the NYC 4S form can result in penalties and interest on any unpaid taxes. The city may also take further action to collect owed taxes. It is advisable to file the form even if the corporation is unable to pay the full amount owed to avoid additional complications.

There are several misconceptions about the NYC 4S form that can lead to confusion for those filing their taxes. Here are four common misunderstandings:

This is not true. The NYC 4S form is designed for general corporations, regardless of their size. Small businesses also need to file this form if they meet the necessary criteria.

Some may think that if they have already paid federal taxes, they do not need to file the NYC 4S form. However, this form is required for corporations operating in New York City, regardless of federal tax obligations.

This is misleading. The NYC 4S form has specific due dates. Late submissions can result in penalties and interest charges, so it is important to file on time.

While there are similarities, the NYC 4S form has unique requirements and calculations specific to New York City. It is essential to complete this form accurately to comply with local tax laws.

Nyks Full Form - Your educational background needs to be documented in the form.

Nys Barber Apprentice Application - Documentation of your infection control course is required with your application.

Here are some key takeaways for filling out and using the NYC 4S form:

After gathering all necessary information and documentation, the next step involves accurately completing the NYC 4S tax return form. This process requires careful attention to detail to ensure compliance with the filing requirements set by the New York City Department of Finance.