Free Nyc 400 Form

Free Nyc 400 Form

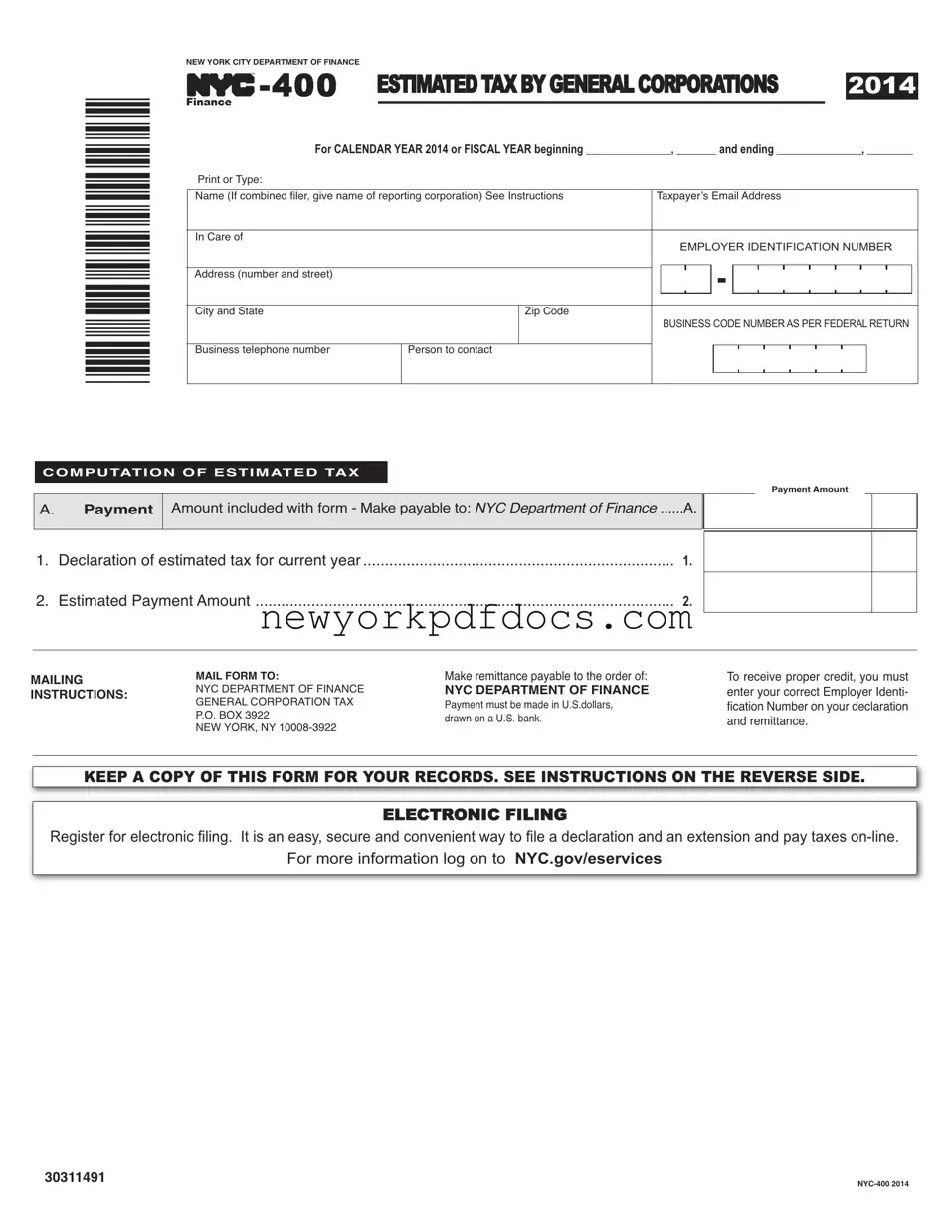

The NYC-400 form is an essential document for corporations operating in New York City that are subject to the General Corporation Tax. This form is used to declare estimated tax payments for the current year, and it is particularly important for businesses that anticipate their tax liability will exceed $1,000. Corporations must complete the form with accurate details, including their Employer Identification Number, business address, and contact information. The form requires taxpayers to calculate their estimated tax based on the previous year’s tax liability, with specific guidelines for installment payments throughout the year. Timely filing is crucial, as late submissions can lead to penalties and immediate payment of all estimated taxes due. Additionally, the NYC Department of Finance encourages electronic filing as a convenient option for submitting the form and managing tax payments. Understanding the requirements and deadlines associated with the NYC-400 can help corporations avoid unnecessary penalties and ensure compliance with local tax laws.

*30311491*

NEWYORK CITYDEPARTMENT OF FINANCE

TM |

ESTIMATEDTAXBYGENERALCORPORATIONS |

2014 |

||||||||||||||||||||||

FINANCE |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For CALENDAR YEAR 2014 or FISCAL YEAR beginning _______________, _______ and ending _______________, ________ |

||||||||||||||||||||||||

Print or Type: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

Name(If combined filer, give name of reporting corporation) See Instructions |

Taxpayer’s EmailAddress |

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

In Care of |

|

|

|

|

EMPLOYER IDENTIFICATION NUMBER |

|||||||||||||||||||

|

|

|

|

|

||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address (number and street) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City and State |

|

|

Zip Code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

BUSINESS CODE NUMBER AS PER FEDERAL RETURN |

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Business telephone number |

|

Person to contact |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

COMPUTATION OF ESTIMATED TAX

Payment Amount

A.Payment

Amount included with form - Make payable to: NYC Department of Finance |

......A. |

|

|

|

|

|

|

|

|

|

|

1. |

Declaration of estimated tax for current year |

1. |

2. |

Estimated PaymentAmount |

2. |

MAILING INSTRUCTIONS:

MAILFORM TO:

NYC DEPARTMENT OF FINANCE GENERAL CORPORATION TAX P.O. BOX 3922

NEW YORK, NY

Make remittance payable to the order of:

NYC DEPARTMENT OF FINANCE

Payment must be made in U.S.dollars, drawn on a U.S. bank.

To receive proper credit, you must enter your correct Employer Identi- ficationNumberonyourdeclaration and remittance.

KEEP A COPY OF THIS FORM FOR YOUR RECORDS. SEE INSTRUCTIONS ON THE REVERSE SIDE.

ELECTRONIC FILING

Registerforelectronicfiling.

For more information log on to NYC.GOV/ESERVICES

30311491

Form |

Page 2 |

|

|

WHOMUSTFILE

Every corporation subject to the NewYork City General CorporationTax (Title 11, Chapter 6, Subchapter 2 of theAdministrative Code) must file a declaration

NOTE:Ifthecurrentyear’staxisreasonablyestimatedtoexceed$1,000,anestimatedpaymentisrequiredevenifthisisthefirstyearofbusi- nessinNewYorkCityforthetaxpayerorthetaxpayerpaidonlytheminimumtaxfortheprecedingyear.Failuretopayorunderpayment ofestimatedtaxinthesecircumstanceswillresultinpenalties.

LINE1 - DECLARATIONOFESTIMATEDTAXFORCURRENTYEAR

Corporationswhosetaxliabilityfortheprecedingyearexceeds$1,000arerequiredtopay,withthetaxreportfortheprecedingyearorwith theapplicationforextensionoftimeforthefilingofsuchreport,25%ofthetaxliabilityfortheprecedingyearasafirstinstallmentofes- timatedtaxforthecurrentyear. Aftertakingcreditforthat25%paymentandfortheamountofanyoverpaymentshownonlastyear’sre- turnwhichthetaxpayerelectedtohaveappliedasacreditagainstthecurrentyear’stax,taxpayersfilingestimatedtaxarerequiredtopay the balance of estimated tax in fractional installments.

ESTIMATEDTAXDUEDATES

Iftherequirementsforfilingestimatedpayments |

Filetheformonorbeforethe: |

Thebalanceofestimatedtaxisdueasfollows: |

arefirstmetduringthetaxableyear: |

|

|

|

|

|

Before the first day of the 6th month |

15th day of the 6th month |

l 1/3 by the 15th day of the 6th month |

|

|

l 1/3 by the 15th day of the 9th month |

|

|

l 1/3 by the 15th day of the 12th month |

|

|

|

On or after the first day of the 6th month and before the |

15th day of the 9th month |

l 1/2 by the 15th day of the 9th month |

first day of the 9th month |

|

l 1/2 by the 15th day of the 12th month |

|

|

|

On or after the first day of the 9th month and before the |

15th day of the 12th month. In lieu of this form, |

Pay in full |

first day of the 12th month |

a completed tax report, with payment of any unpaid |

|

|

balance of tax, may be filed on or before the 15th day |

|

|

of the 2nd month of the following year. |

|

|

|

|

If any of the above dates fall on a Saturday, Sunday or legal holiday, the due date is the next business day.

AMENDMENTS

LATEFILING

PENALTY

The law imposes penalties for failure to pay or underpayment of estimated tax. (Refer to Section

istrative Code.)

ELECTRONICFILING

Note: Register for electronic filing. It is an easy, secure and convenient way to file and pay an extension

For more information log on to NYC.gov/eservices

Filling out the NYC-400 form can be a straightforward process, but many people make common mistakes that can lead to delays or penalties. Here are nine mistakes to avoid when completing this important document.

One frequent error is failing to provide the correct Employer Identification Number (EIN). This number is crucial for identifying your business. If you enter an incorrect EIN, your form may be rejected, causing unnecessary complications. Always double-check this number against your federal return to ensure accuracy.

Another common mistake is not including the estimated payment amount. The form requires you to declare how much you estimate you will owe for the current year. Forgetting to fill this in can result in penalties. Make sure to calculate your estimated tax accurately based on the previous year’s liability.

People often overlook the mailing instructions. It’s essential to send your form to the correct address, which is the NYC Department of Finance. Sending it elsewhere can lead to delays in processing your payment. Always verify the mailing address before sending your form.

Some individuals fail to keep a copy of the form for their records. Keeping a copy is vital for future reference, especially if there are any discrepancies. This simple step can save you time and stress later on.

Another mistake is missing the filing deadlines. The NYC-400 has specific due dates for estimated tax payments. If you miss these deadlines, you may face penalties and interest charges. Mark your calendar and set reminders to ensure timely submission.

Many filers also forget to sign and date the form. An unsigned form is considered incomplete and may not be processed. Always remember to sign and date your form before mailing it.

Some people incorrectly assume that they do not need to file if it’s their first year in business. Even if it’s your first year, you must file if your estimated tax exceeds $1,000. Ignoring this requirement can lead to penalties, so be sure to file regardless of your business history.

Another common issue is not updating business information. If your address, business name, or other details have changed, make sure to reflect those changes on the form. Outdated information can cause confusion and delays in processing.

Lastly, many individuals neglect to register for electronic filing. This method is often easier and more efficient. It allows you to file and pay online, reducing the chances of errors. Consider registering for electronic filing to simplify the process.

By being aware of these common mistakes, you can ensure that your NYC-400 form is filled out correctly and submitted on time, helping you avoid unnecessary penalties and complications.

The NYC-400 form is a declaration of estimated tax for corporations subject to the New York City General Corporation Tax. Corporations must file this form if they expect their estimated tax for the current year to exceed $1,000. It helps the city collect taxes from businesses operating within its jurisdiction.

Every corporation that is subject to the New York City General Corporation Tax must file the NYC-400 if its estimated tax for the current year is expected to exceed $1,000. This requirement holds true even if it is the corporation's first year of business in New York City or if it only paid the minimum tax in the previous year.

The due dates for filing the NYC-400 form depend on when the requirements for filing estimated payments are first met during the taxable year. Generally, the form must be filed before the first day of the 6th month of the tax year, with subsequent payments due on the 15th of the 6th, 9th, and 12th months.

Payments must be made in U.S. dollars and drawn on a U.S. bank. You should make your remittance payable to the NYC Department of Finance. It's important to include your correct Employer Identification Number (EIN) on both the declaration and your payment to ensure proper credit.

If the NYC-400 form is filed after the due date, all installments of estimated tax due must be paid at once. Remaining installments will be due as if the form had been filed on time. Late filing can lead to penalties, so it's best to adhere to the deadlines.

Yes, you can file an amended NYC-400 form if you need to correct your tax estimate or related payments. If you make an amendment after the 15th day of the 9th month of the taxable year, any increase in tax must be paid with the amendment.

The law imposes penalties for failure to pay or underpayment of estimated tax. It's important to stay informed about these penalties to avoid unexpected costs. Refer to Section 11-676 of the Administrative Code for specific details.

Yes, electronic filing is available and is considered an easy, secure, and convenient way to file the NYC-400 form and pay taxes online. For more information, you can visit NYC.gov/eservices.

You should mail the completed NYC-400 form to the NYC Department of Finance, General Corporation Tax, P.O. Box 3922, New York, NY 10008-3922. Ensure that you keep a copy of the form for your records.

There are several misconceptions surrounding the NYC 400 form that can lead to confusion for corporations required to file. Below are five common misunderstandings, along with clarifications for each.

In reality, any corporation that expects its estimated tax for the current year to exceed $1,000 must file this form, regardless of its size. This includes smaller businesses that may be just starting out.

Some believe that new businesses do not need to file the NYC 400 form in their first year. However, if the estimated tax exceeds $1,000, they are required to file, even if it is their first year operating in New York City.

This is incorrect. The law imposes penalties for late payments or underpayment of estimated tax. Timely filing and payment are crucial to avoid additional charges.

Corporations that may not have made a profit can still be required to file if they anticipate their estimated tax will exceed $1,000. It is based on estimates, not actual profit.

While electronic filing is convenient and secure, it is also important to register for it in advance. Doing so helps ensure that the filing and payment process is completed on time.

Ny State Tax Percentage - Overall, the IT-200 is crucial for residents to fulfill their state tax obligations.

Nyc-1127 - Be sure to check the special condition codes applicable for your tax situation when submitting.

Primary Beneficiary Designation - The completed form ensures a smoother process for your beneficiaries when claiming death benefits.

Filling out the NYC-400 form is an essential task for corporations subject to New York City's General Corporation Tax. Here are some key takeaways to keep in mind:

By understanding these key points, corporations can navigate the filing process more effectively and avoid unnecessary complications.

Completing the NYC-400 form is an essential step for corporations subject to the New York City General Corporation Tax. This process requires careful attention to detail to ensure accuracy and compliance with local tax regulations. After filling out the form, it must be submitted to the NYC Department of Finance along with the appropriate payment.

After submitting the form, ensure to monitor any correspondence from the NYC Department of Finance for confirmation or additional instructions. Timely filing and payment are crucial to avoid penalties.