Free Nyc 204 Form

Free Nyc 204 Form

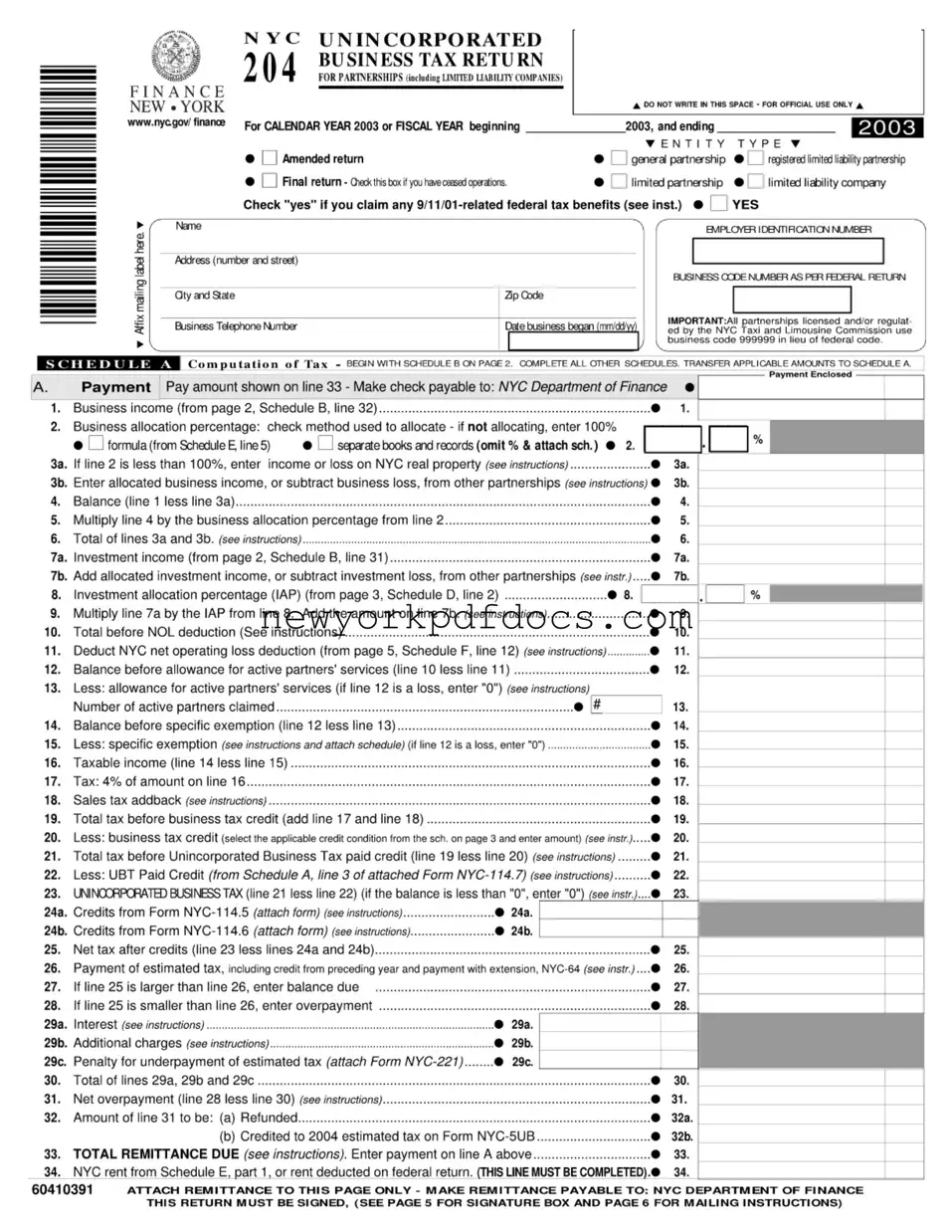

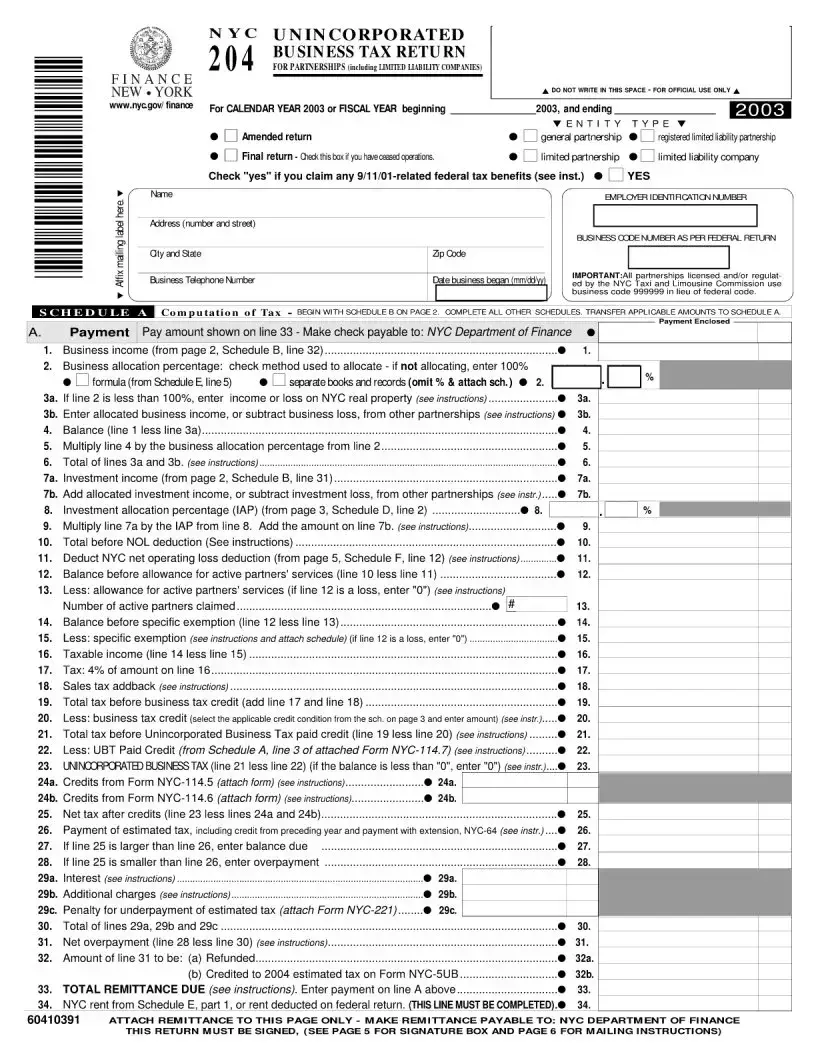

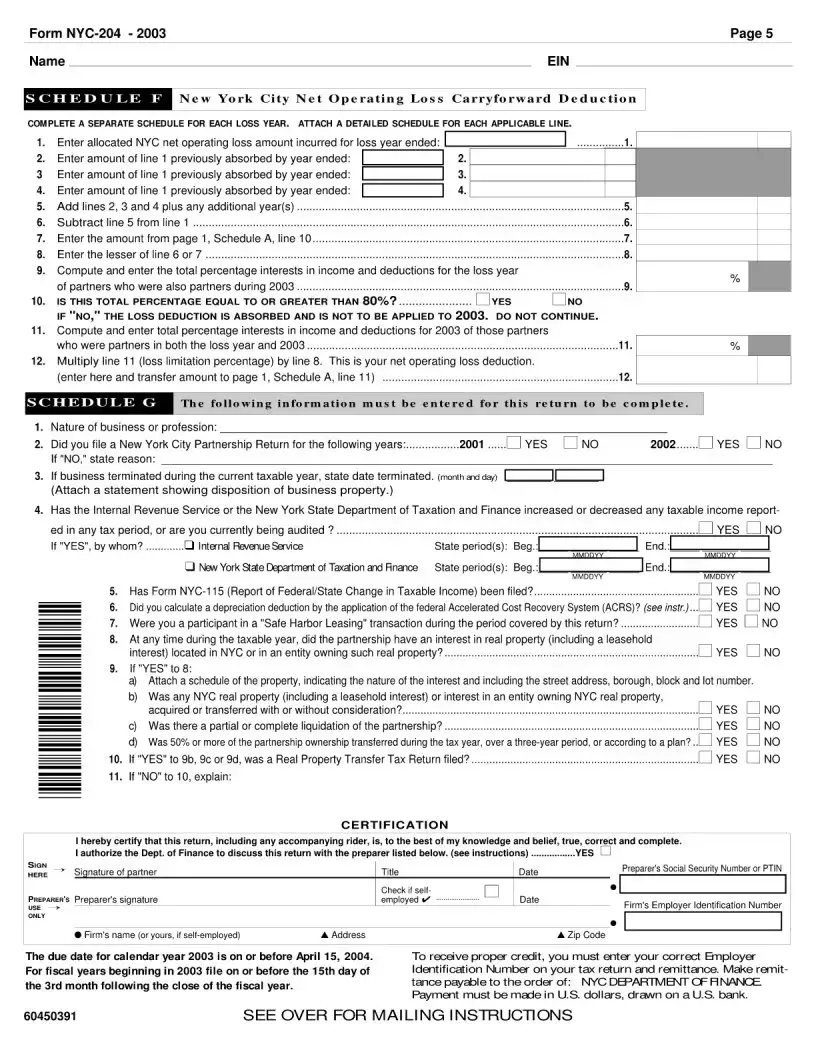

The NYC 204 form is a crucial document for partnerships, including limited liability companies, operating within New York City. It serves as the Unincorporated Business Tax (UBT) return, allowing these entities to report their income and calculate the taxes owed to the city. The form is designed for use by partnerships that have either a calendar year or fiscal year ending in 2003. It includes sections for detailing business income, allocation percentages, and various deductions. Notably, the form requires partnerships to specify if they are claiming any federal tax benefits related to the events of September 11, 2001. Additionally, it encompasses a comprehensive breakdown of taxable income, investment income, and the applicable tax rates. The NYC 204 also provides for credits and deductions, enabling partnerships to reduce their tax liability. Completing this form accurately is essential, as it ensures compliance with city regulations and helps avoid potential penalties. Thus, understanding the components and requirements of the NYC 204 form is vital for any partnership engaged in business activities within New York City.

Form 1065: This is the U.S. Return of Partnership Income. Like the NYC 204 form, it is used by partnerships to report income, deductions, and other tax-related information. Both forms require a detailed account of income sources and allocations among partners.

Schedule K-1: This document is used to report each partner's share of income, deductions, and credits from the partnership. Similar to the NYC 204, it provides detailed information that partners need for their individual tax returns.

Form 1120: This is the U.S. Corporation Income Tax Return. While it applies to corporations, it shares similarities with the NYC 204 in terms of reporting income and calculating tax liabilities, albeit for a different type of entity.

Form NYC-114: This is used for claiming business tax credits in New York City. The NYC 204 form requires information on tax credits, making the NYC-114 relevant for partnerships seeking to reduce their tax burden.

Form NYC-64: This is the application for a business extension in New York City. Similar to the NYC 204, it involves reporting financial information and can affect the timing of tax payments.

Schedule E: This is used to report supplemental income and loss, which can include income from partnerships. Both the NYC 204 and Schedule E require detailed income reporting, making them closely related.

Form 1040: This is the U.S. Individual Income Tax Return. While it is for individuals, it includes information from partnerships reported on Schedule K-1, which is similar to the income reporting required on the NYC 204.

Form NYC-114.7: This form is used to report Unincorporated Business Tax (UBT) paid credits. The NYC 204 references this form for calculating tax credits, highlighting the interconnectedness of these documents.

Filling out the NYC 204 form can be a straightforward process, but several common mistakes can lead to complications. One frequent error occurs when individuals fail to check the appropriate boxes for their return type. Whether it is an amended return or a final return, neglecting to mark these options can result in delays or rejections of the submission.

Another common mistake is not providing accurate business income figures. Many people either miscalculate their income or fail to include all relevant sources. This oversight can significantly affect the overall tax liability. It is essential to review all income sources thoroughly and ensure they are reported correctly on the form.

Additionally, some filers forget to include their Employer Identification Number (EIN). This number is crucial for identifying the business and ensuring that the tax return is processed correctly. Without it, the NYC Department of Finance may not be able to link the return to the correct entity, leading to potential issues down the line.

Another area where errors frequently occur is in the allocation percentage. Many partnerships do not check the method they used to allocate income, which can lead to incorrect calculations. It is important to understand the options available and select the appropriate method based on the partnership's specific circumstances.

Moreover, failing to sign the form is a mistake that can easily be overlooked. A signature is required to validate the return, and without it, the submission is considered incomplete. This simple step is often forgotten in the rush to meet deadlines.

Lastly, individuals sometimes neglect to attach the necessary schedules or documentation. Each section of the form may require additional information to support the reported figures. Ensuring that all required attachments are included can prevent unnecessary delays and complications with the processing of the return.

The NYC 204 form is the Unincorporated Business Tax Return specifically designed for partnerships and limited liability companies operating in New York City. This form is used to report income, deductions, and calculate the tax owed to the city for the business activities conducted during the tax year.

Any partnership or limited liability company that conducts business in New York City and meets the income threshold must file the NYC 204 form. This includes general partnerships, registered limited liability partnerships, limited partnerships, and limited liability companies. If your business has ceased operations, you should check the box for a final return.

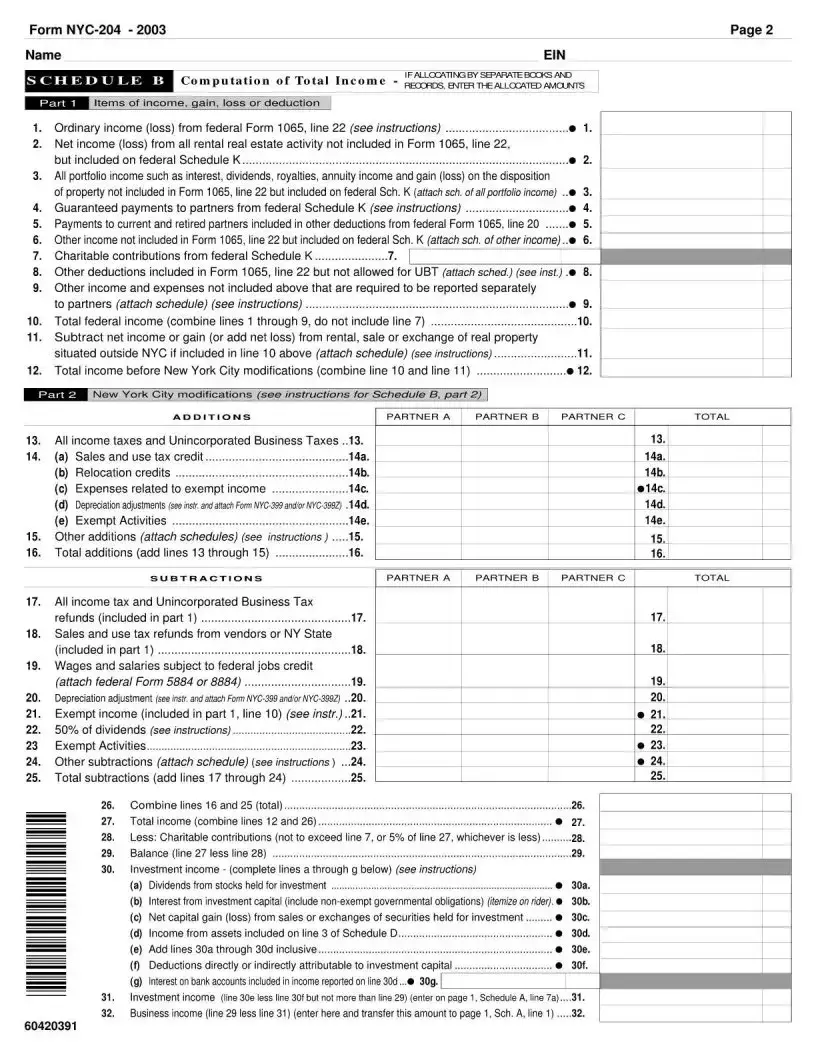

To calculate your taxable income, start with your total business income. From there, you will make necessary adjustments, including deductions for losses, expenses related to exempt income, and other specific exemptions. The final figure after all deductions will be your taxable income, which is used to calculate the Unincorporated Business Tax.

The NYC 204 form is typically due on the 15th day of the fourth month following the end of your fiscal year. For those on a calendar year, this means the form is due on April 15. If you need more time, you can file for an extension, but you must pay any estimated tax owed by the original due date to avoid penalties.

If you discover an error after submitting your NYC 204 form, you should file an amended return. Indicate that it is an amended return and provide the correct information. It’s important to address mistakes promptly to avoid potential penalties or interest on unpaid taxes.

This form is specifically designed for unincorporated businesses, including partnerships and limited liability companies. It applies to any entity that operates as a partnership in New York City.

Even if a partnership has no income, it is still required to file the NYC 204 form. Filing is necessary to report the business's status and comply with local regulations.

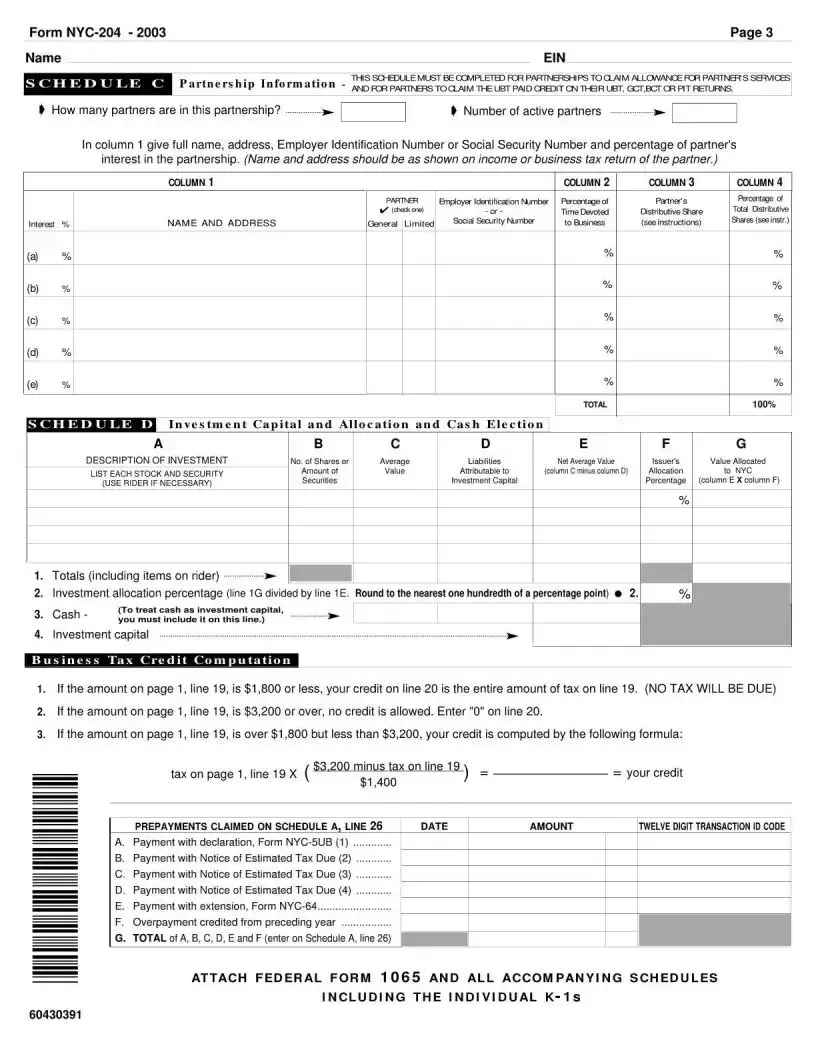

Partnerships must choose an appropriate method for income allocation based on their specific circumstances. Options include using a formula or maintaining separate books and records.

While the NYC 204 form is related to federal filings, it has distinct requirements and calculations specific to New York City. It is important to complete both forms accurately.

It is mandatory to sign the NYC 204 form before submission. A signature verifies the accuracy of the information provided and fulfills legal requirements.

Maintaining accurate records is crucial. Partnerships must keep detailed records of income, expenses, and allocation methods to support the information reported on the form.

Limited liability companies operating as partnerships are required to file the NYC 204 form just like any other partnership. Compliance is essential for avoiding penalties.

How Much Is Ambulance Ride Nyc - A check or money order for $1.50 is necessary for each report requested.

New York State Employee Health Insurance Premiums - The completed form should be sent to the New York State Department of Civil Service.

When filling out the NYC 204 form, here are some key takeaways to keep in mind:

By keeping these points in mind, you can navigate the NYC 204 form more effectively and ensure compliance with local tax regulations.

Completing the NYC 204 form is an essential task for partnerships operating within New York City. This form is used to report business income and calculate the Unincorporated Business Tax (UBT). Before starting, ensure you have all necessary financial documents on hand, including income statements and any relevant schedules. Here’s a straightforward guide to help you fill out the form accurately.