Free Ny Et 141 Form

Free Ny Et 141 Form

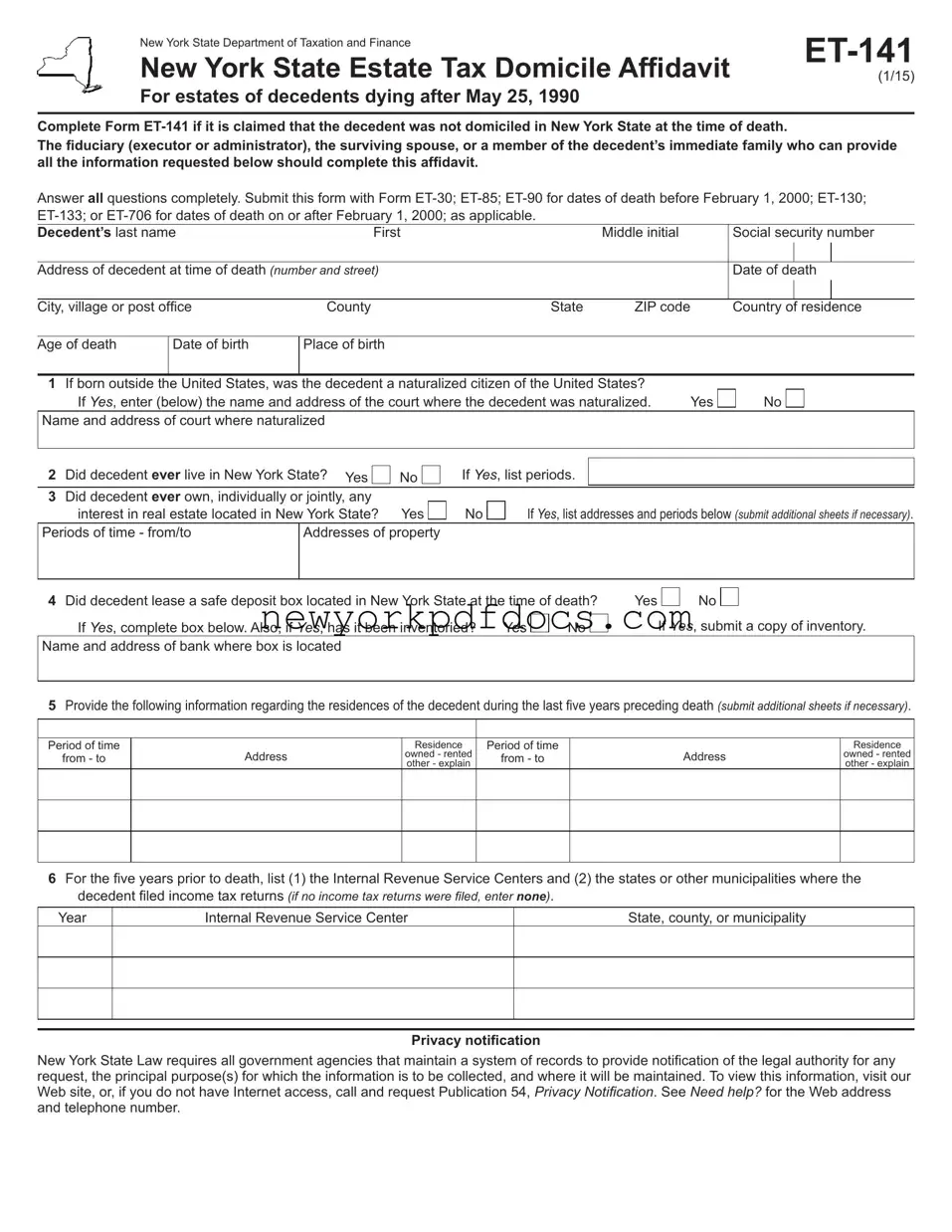

The NY ET-141 form, officially known as the New York State Estate Tax Domicile Affidavit, plays a crucial role in estate tax matters for individuals who have passed away after May 25, 1990. This form is essential when claiming that the decedent was not a resident of New York State at the time of their death. It must be filled out by the fiduciary, such as the executor or administrator, or by a close family member who can provide accurate information. The form requires detailed responses to various questions, including the decedent's personal information, residency history, and any real estate interests in New York. It also asks about the decedent's voting history, employment, and any legal proceedings they may have been involved in within the state. Supporting documents may be necessary to substantiate claims made in the affidavit. This form must be submitted alongside other relevant tax forms, depending on the date of death. Completing the NY ET-141 accurately is vital for a smooth estate tax process and can significantly affect the outcome of the estate's tax obligations.

New York State Department of Taxation and Finance |

||

New York State Estate Tax Domicile Afidavit |

||

(1/15) |

For estates of decedents dying after May 25, 1990

Complete Form

The iduciary (executor or administrator), the surviving spouse, or a member of the decedent’s immediate family who can provide all the information requested below should complete this afidavit.

Answer all questions completely. Submit this form with Form

Decedent’s last name |

First |

|

|

|

|

Middle initial |

|

Social security number |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address of decedent at time of death (number and street) |

|

|

|

|

|

|

|

Date of death |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City, village or post ofice |

County |

|

|

|

State |

ZIP code |

|

Country of residence |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Age of death |

Date of birth |

Place of birth |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

1 |

If born outside the United States, was the decedent a naturalized citizen of the United States? |

|

|

|

|

||||||||

|

If Yes, enter (below) the name and address of the court where the decedent was naturalized. |

Yes |

No |

||||||||||

Name and address of court where naturalized |

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

||

|

Did decedent ever live in New York State? Yes |

|

|

|

|

|

|

|

|

||||

2 |

No |

If Yes, list periods. |

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

Did decedent ever own, individually or jointly, any |

|

|

|

If Yes, list addresses and periods below (submit additional sheets if necessary). |

||||||||

|

interest in real estate located in New York State? |

Yes |

No |

|

|||||||||

Periods of time - from/to |

Addresses of property |

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

||||

4 |

Did decedent lease a safe deposit box located in New York State at the time of death? |

Yes |

No |

|

|

|

|||||||

|

If Yes, complete box below. Also, if Yes, has it been inventoried? |

Yes |

No |

If Yes, submit a copy of inventory. |

|||||||||

Name and address of bank where box is located |

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5Provide the following information regarding the residences of the decedent during the last ive years preceding death (submit additional sheets if necessary).

Period of time

from - to

Address

Residence

owned - rented other - explain

Period of time

from - to

Address

Residence

owned - rented other - explain

6For the ive years prior to death, list (1) the Internal Revenue Service Centers and (2) the states or other municipalities where the decedent iled income tax returns (if no income tax returns were iled, enter NONE).

Year

Internal Revenue Service Center

State, county, or municipality

Privacy notiication

New York State Law requires all government agencies that maintain a system of records to provide notiication of the legal authority for any

request, the principal purpose(s) for which the information is to be collected, and where it will be maintained. To view this information, visit our Web site, or, if you do not have Internet access, call and request Publication 54, Privacy Notiication. See Need help? for the Web address

and telephone number.

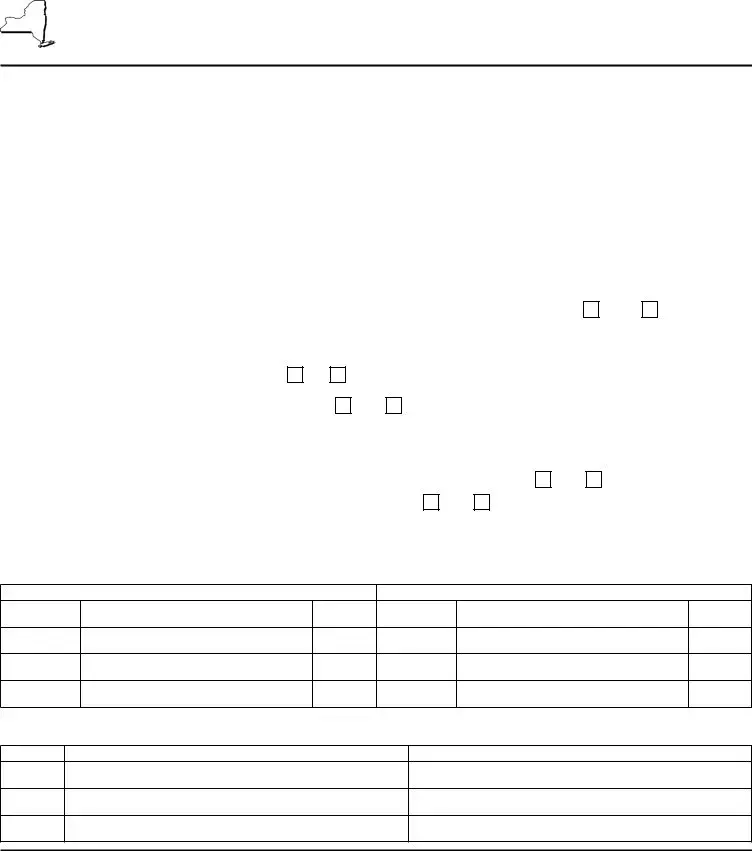

7List the states where the decedent was registered to vote during the last ive years preceding death (list latest year irst).

Years |

|

State |

|

|

|

|

|

From |

|

To |

|

|

|

|

|

|

|

Date of Death |

|

|

|

|

|

|

|

|

|

|

|

|

|

If decedent did not vote in those ive years, when did he or she last vote? |

|

Where? |

|

|

|

8List employment or business activities (if any) engaged in by the decedent during the ive years preceding the date of death.

|

|

|

In New York State |

|

|

|

|

|

Outside New York State |

|

|||

Period of time |

|

Nature of employment or business activities |

Period of time |

|

Nature of employment or business activities |

||||||||

|

from - to |

|

from - to |

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

9 |

Was decedent a party to any legal proceedings in New York State during the last ive years? |

Yes |

No |

If Yes, list courts, dates, |

|||||||||

and types of action. |

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

10 |

Did decedent have a license to operate a business, profession, motor vehicle, airplane, or boat? |

Yes |

No |

If Yes, list below. |

|||||||||

|

License number |

|

Type of license |

Date of issuance |

|

|

|

Name and location of issuing ofice |

|||||

|

|

|

|

|

|

|

|

|

|||||

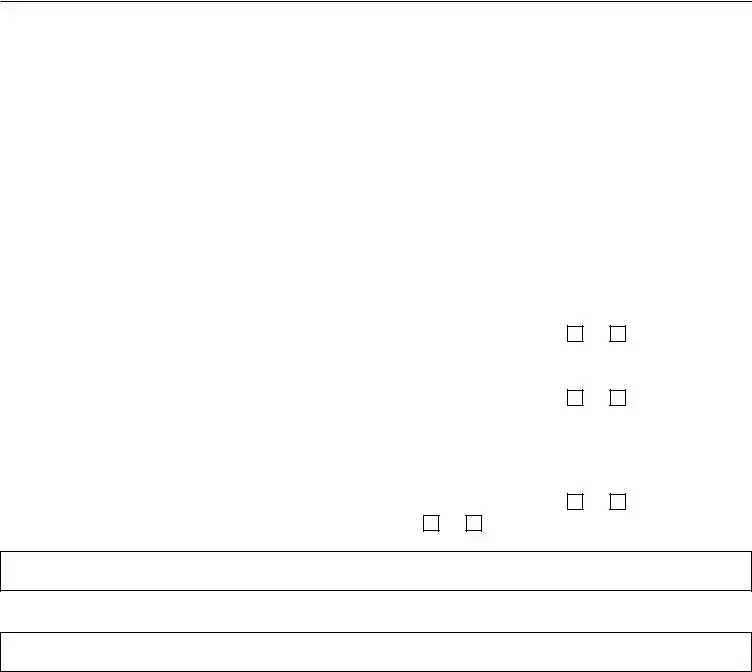

11 |

Did decedent execute any trust indentures, deeds, mortgages, or any other documents |

|

|

|

|

||||||||

|

describing his or her residence during the last ive years preceding death? |

|

|

|

Yes |

No |

If Yes, submit a copy. |

||||||

12 |

Was the decedent a member of any church, club, or organization? |

Yes |

No |

|

|

|

|

||||||

If Yes, give name, address, and other details. (Submit additional sheets if necessary.)

13What other information do you wish to submit in support of the contention that the decedent was not domiciled in New York State at the time of death? (Submit additional sheets if necessary.)

Applicant’s last name |

First name |

Middle initial |

Relationship to decedent |

|

|

|

|

Address (number and street) |

|

|

Connection with estate |

|

|

|

|

City, village, or post ofice |

State |

ZIP code |

Country of residence |

|

|

|

|

The undersigned states that this afidavit is made to induce the Commissioner of the Department of Taxation and Finance of the State of New York to determine

domicile, and that the answers herein contained to the foregoing questions are each and every one of them true in every particular.

|

|

|

|

|

|

|

Signature of Notary Public, Commissioner of Deeds or Authorized New York State |

|

Signature of applicant |

|

|

|

|

|

Department of Taxation and Finance employee (no seal required) |

||

Sworn before me this |

|

|

day of |

|

20 |

|

|

|

|

|

|

|

|

|

|

Signature |

|

Filling out the NY ET-141 form can be a straightforward process, but many people make mistakes that can lead to delays or complications. One common error is incomplete answers. Each question on the form requires a thorough response. Leaving any section blank or providing vague answers can raise red flags and may result in the form being rejected. It is crucial to ensure that all questions are answered completely and accurately.

Another frequent mistake involves incorrect documentation. Applicants often forget to include necessary supporting documents when submitting the form. For instance, if the decedent had a safe deposit box, a copy of the inventory must be provided. Failing to include these documents can lead to further inquiries and prolong the review process.

Additionally, many individuals overlook the importance of listing all relevant residences during the last five years prior to the decedent's death. This section is vital for establishing domicile. If the decedent lived in multiple locations, it is essential to provide detailed information for each residence, including ownership status and duration of stay. Omitting any residences can affect the outcome of the domicile determination.

Lastly, some applicants do not pay close attention to signature requirements. The form must be signed by the applicant and may also require notarization. Neglecting to sign or improperly completing the signature section can result in the form being deemed invalid. Ensuring that all signatures are in place is a critical step in the submission process.

The NY ET-141 form is used to claim that a decedent was not domiciled in New York State at the time of death. This affidavit must be completed by the fiduciary, surviving spouse, or a member of the decedent's immediate family who can provide the necessary information.

The form should be completed by the fiduciary (executor or administrator), the surviving spouse, or a close family member of the decedent who has access to the required information.

This form must be submitted along with other relevant forms such as ET-30, ET-85, ET-90, ET-130, ET-133, or ET-706, depending on the date of death of the decedent.

The form requires details such as the decedent's full name, social security number, address at the time of death, date of birth, place of birth, and residency history. It also asks about real estate ownership, tax filings, voting registration, and other pertinent information.

Yes, the form specifically requests residency information for the five years preceding the decedent's death. This includes addresses, ownership status, and any other relevant details.

If the decedent lived in New York State, the form requires you to list the periods of residence and any real estate owned during that time. This information is crucial for establishing domicile.

Yes, the New York State Law mandates that all government agencies provide notification regarding the collection of personal information. You can view this information on the New York State Department of Taxation and Finance website or request it via phone.

If you have more information to support your claim that the decedent was not domiciled in New York State, you may submit additional sheets along with the completed form.

The form must be signed by the applicant and notarized. The signature of a notary public, commissioner of deeds, or an authorized employee of the New York State Department of Taxation and Finance is also required.

After submission, the New York State Department of Taxation and Finance will review the affidavit and the accompanying documents to determine the decedent's domicile status for estate tax purposes.

Understanding the NY ET-141 form is crucial for anyone involved in estate matters in New York State. However, several misconceptions can lead to confusion. Here are six common misunderstandings about this form:

This is not true. The form is required for any estate where the decedent's domicile is in question, regardless of the estate's value.

While attorneys can assist, the form can be filled out by the fiduciary, surviving spouse, or immediate family members who have the necessary information.

Completing the form is mandatory if there is a claim that the decedent was not domiciled in New York at the time of death, regardless of their residence history.

While it is important to provide complete information, if a question does not apply, it is acceptable to indicate that with a clear response.

Supporting documents are often necessary to substantiate claims made on the form, especially regarding real estate and residency.

In fact, if errors are discovered after submission, it is possible to amend the form. Contact the New York State Department of Taxation and Finance for guidance on this process.

Does My Zip Code Qualify for Free Solar Panels - Consult the detailed instructions if you have specific questions or concerns.

Nyc Pension - Your acknowledgment before a Notary is necessary for the form's validity.

Nyc 210 - Fill out your city, state, ZIP code, and country if not in the U.S.

When completing the NY ET-141 form, there are several important points to keep in mind:

Gathering all necessary information and documentation before starting can streamline the process and help ensure accuracy.

Completing the NY ET-141 form is essential for establishing that a decedent was not domiciled in New York State at the time of death. This affidavit must be filled out accurately and submitted alongside other relevant forms. The following steps will guide you through the process of filling out the form correctly.

After completing the form, ensure that all information is accurate and that any required supporting documents are included. Submit the NY ET-141 form along with the appropriate accompanying forms to the New York State Department of Taxation and Finance for processing.