Free New York Et 133 Form

Free New York Et 133 Form

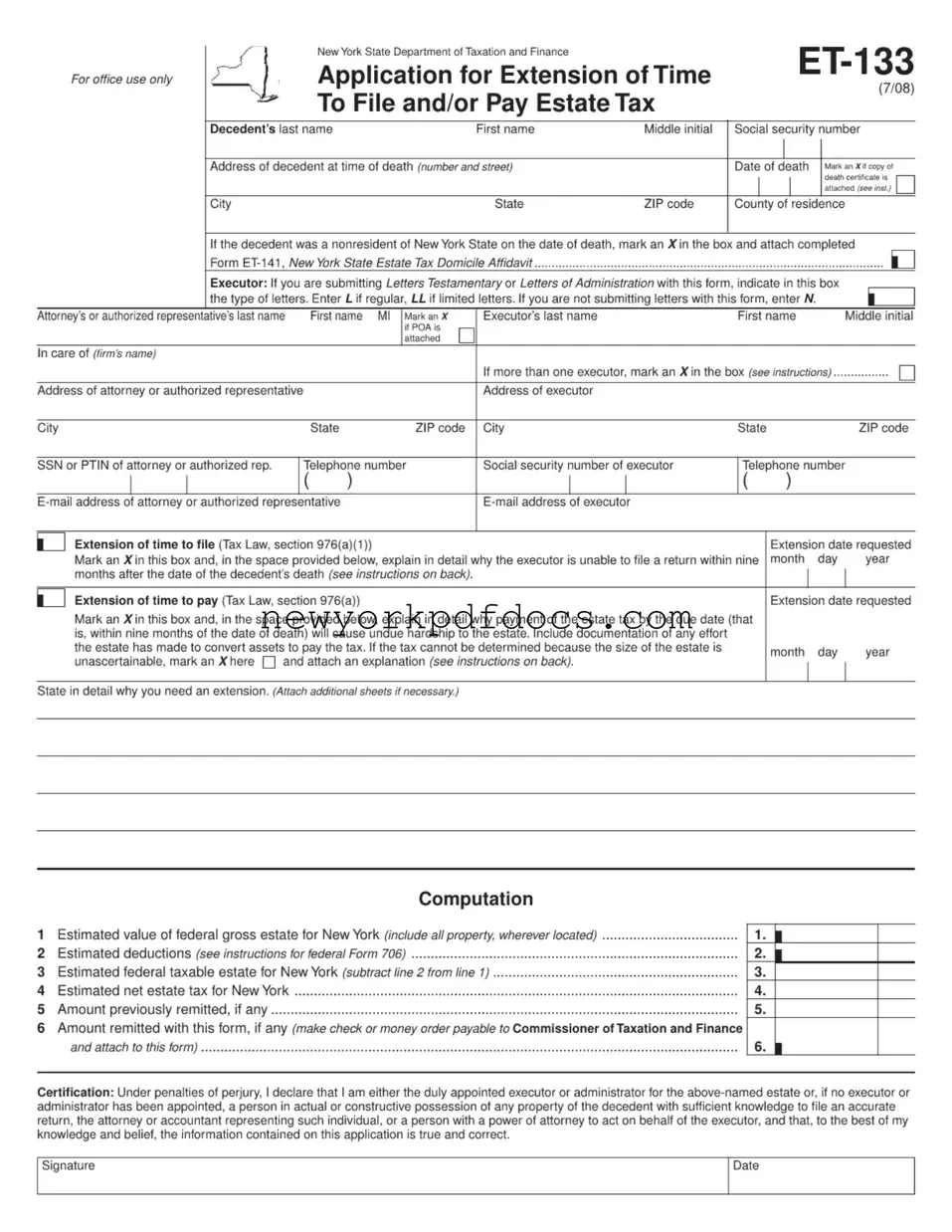

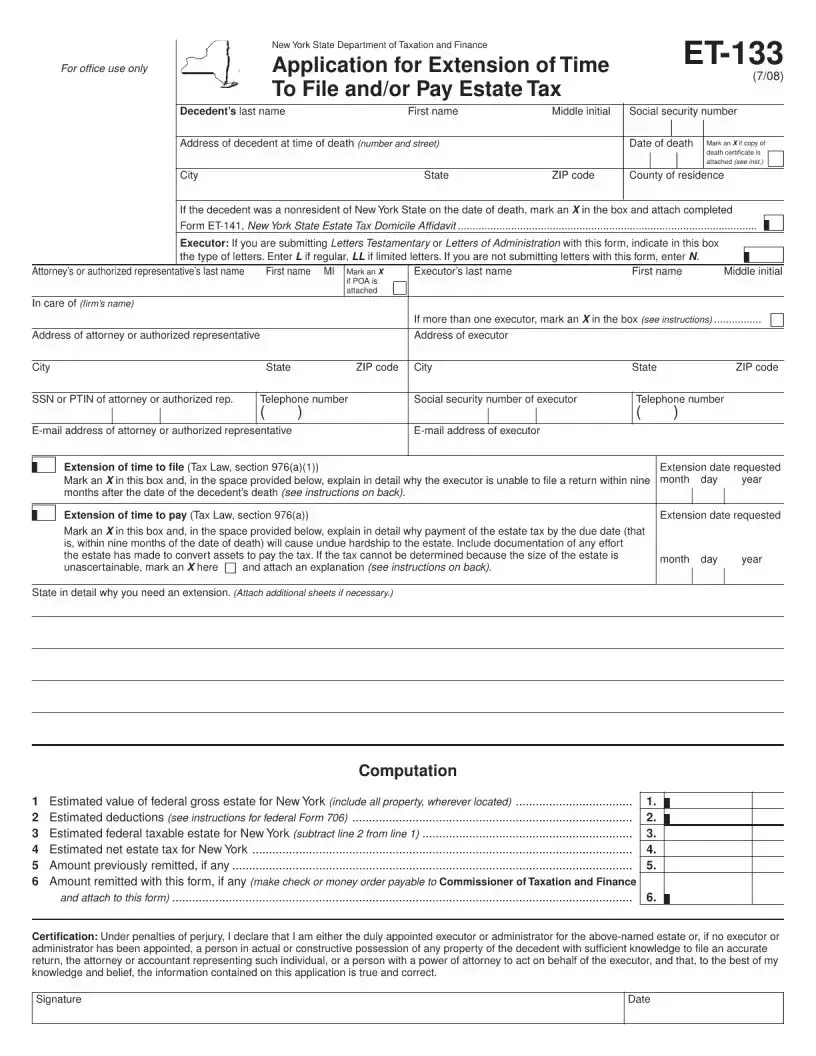

The New York ET-133 form serves as a vital tool for executors of estates, allowing them to request an extension of time to file or pay estate taxes. This application is particularly important when circumstances make it difficult to meet the original deadlines set by the state. Executors must provide essential information about the decedent, including their name, social security number, and address at the time of death, as well as the date of death. If the decedent was a nonresident, additional documentation is required. The form also prompts executors to explain the reasons for their request for an extension, whether it be for filing or payment. This explanation must detail the hardships that would arise from adhering to the standard nine-month deadline. Furthermore, the ET-133 form allows for the inclusion of authorized representatives, such as attorneys or accountants, who can act on behalf of the executor. The form must be submitted within nine months of the decedent’s passing to avoid penalties, and it is crucial for executors to ensure that all necessary documentation, including death certificates and letters of administration, are attached to facilitate the review process by the New York State Department of Taxation and Finance. Understanding the nuances of this form can significantly ease the burden during a challenging time, helping to ensure compliance with state tax laws while allowing for the necessary time to manage the estate properly.

Form ET-141, New York State Estate Tax Domicile Affidavit: This form is used when a decedent was a nonresident of New York at the time of death. Similar to the ET-133, it requires detailed information about the decedent and is necessary for establishing the estate's tax obligations in New York.

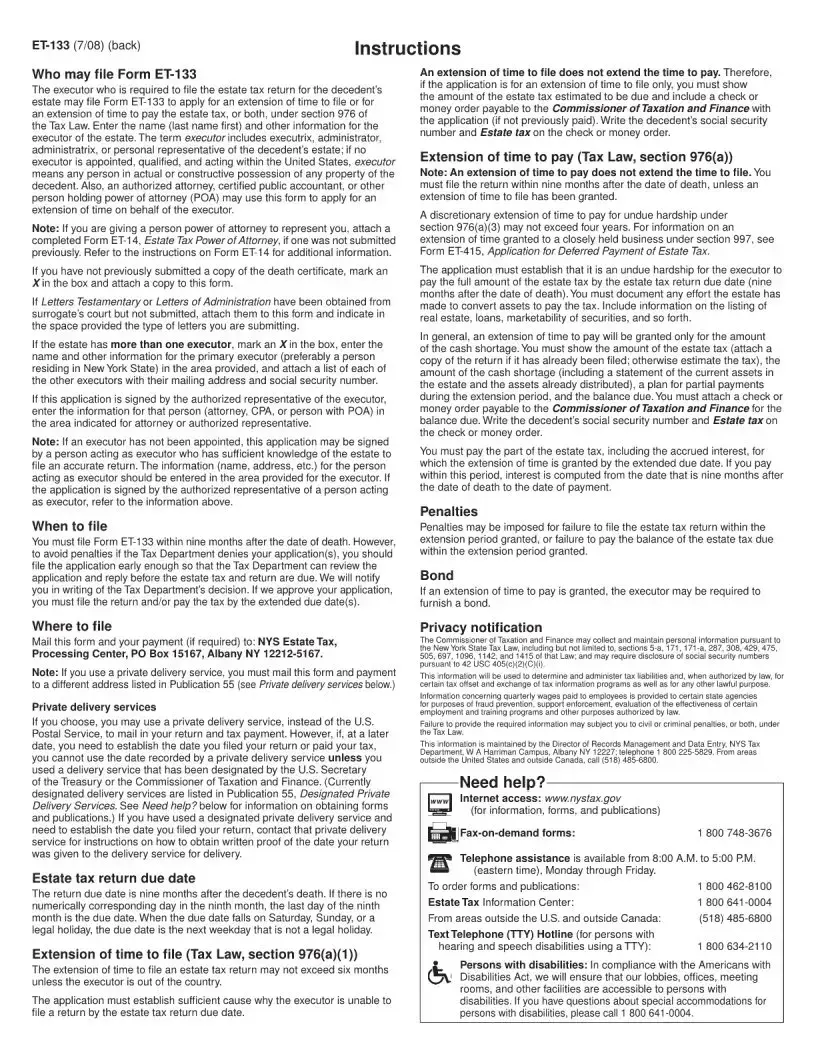

Form ET-14, Estate Tax Power of Attorney: This document allows an individual to authorize someone else to act on their behalf regarding estate tax matters. Like the ET-133, it involves the executor's information and requires signatures to validate the authority granted.

Form 706, United States Estate (and Generation-Skipping Transfer) Tax Return: The federal equivalent of the ET-133, Form 706 is used to report estate taxes at the federal level. Both forms require detailed information about the decedent's assets and liabilities, and both can be filed to request extensions for filing or payment.

Form 2848, Power of Attorney and Declaration of Representative: This form is used to appoint someone to represent you before the IRS. Similar to the ET-14, it is relevant in estate tax matters and requires similar personal and representative information, ensuring that the appointed person can handle tax-related issues.

Filling out the New York ET-133 form can be a daunting task, and mistakes can lead to delays or complications. One common error is failing to attach the death certificate. If you haven't previously submitted a copy, it is crucial to mark the box indicating that the certificate is attached. This step is essential for the processing of your application and helps ensure that the Tax Department has all necessary documentation on file.

Another frequent mistake involves incomplete information regarding the executor. The form requires specific details, such as the executor's name, address, and social security number. If there is more than one executor, it's important to mark the appropriate box and provide a list of all executors, including their mailing addresses and social security numbers. Omitting this information can result in your application being rejected or delayed.

Additionally, many individuals overlook the section where they must explain the reasons for requesting an extension. Simply marking the box is not sufficient. You must provide a detailed explanation of why filing or payment cannot occur within the standard nine-month period. This explanation should include any efforts made to convert estate assets to pay the tax. Without a clear rationale, the Tax Department may not grant your request.

Providing inaccurate or outdated contact information for the attorney or authorized representative is another common pitfall. Ensure that the address, phone number, and email address are current. This information is vital for communication regarding your application. If the Tax Department needs to reach out for clarification or additional documentation, having accurate contact details can expedite the process.

Finally, neglecting to sign and date the application is a critical oversight. The certification section requires the executor or authorized representative to declare the truthfulness of the information provided. Without a signature, the application cannot be processed. Always double-check that all required fields are completed and that the form is signed before submission.

The New York ET-133 form is used to request an extension of time to file or pay estate tax. Executors of an estate can submit this form if they need more time beyond the standard nine months after the decedent's death. This form helps ensure that the estate tax return and payment can be completed accurately and without undue pressure.

The executor or administrator of the decedent's estate is eligible to file the ET-133 form. If no executor has been appointed, any person in possession of the decedent's property can file. Additionally, an authorized attorney or representative with a power of attorney can submit the form on behalf of the executor.

You must file the ET-133 form within nine months after the date of the decedent's death. To avoid penalties, it is best to file the form early enough for the Tax Department to review it and respond before the estate tax return and payment are due.

After you submit the ET-133 form, the Tax Department will notify you in writing of their decision regarding your request for an extension. If your application is approved, you will receive a new due date for filing the estate tax return and/or making the tax payment.

You should mail the completed ET-133 form and any required payment to the NYS Estate Tax Processing Center at PO Box 15167, Albany NY 12212-5167. If you use a private delivery service, be sure to check the specific address listed in Publication 55, as it may differ from the one for standard mail.

Misconceptions about the New York ET-133 form can lead to confusion for executors and representatives. Here are eight common misunderstandings, along with clarifications to help you navigate the process more smoothly.

Understanding these misconceptions can help ensure that you complete the ET-133 form correctly and in a timely manner. Always refer to the official instructions or consult with a professional if you have specific questions.

Filling out and using the New York ET-133 form is a critical step for executors managing estate tax obligations. Here are key takeaways to consider:

Completing the New York ET-133 form is an essential step for those seeking an extension of time to file or pay estate tax. After filling out the form, it should be submitted to the appropriate tax authority within nine months of the decedent's death. Ensure that all required information is accurate and complete to avoid delays in processing your request.

Once the form is completed, it should be mailed to the NYS Estate Tax Processing Center. If you are using a private delivery service, please refer to the specific guidelines to ensure timely processing. Remember to keep copies of all documents for your records.