Free New York 810 Form

Free New York 810 Form

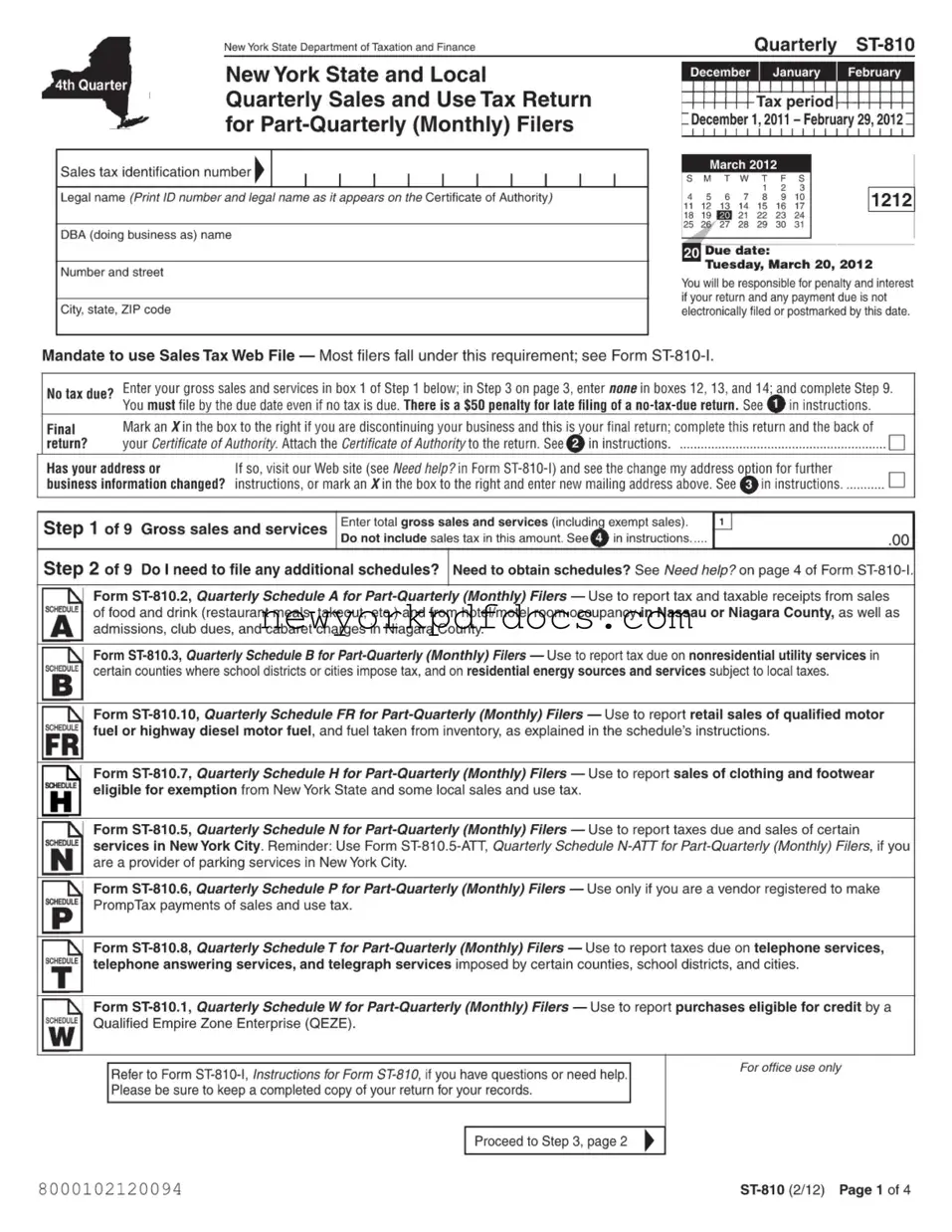

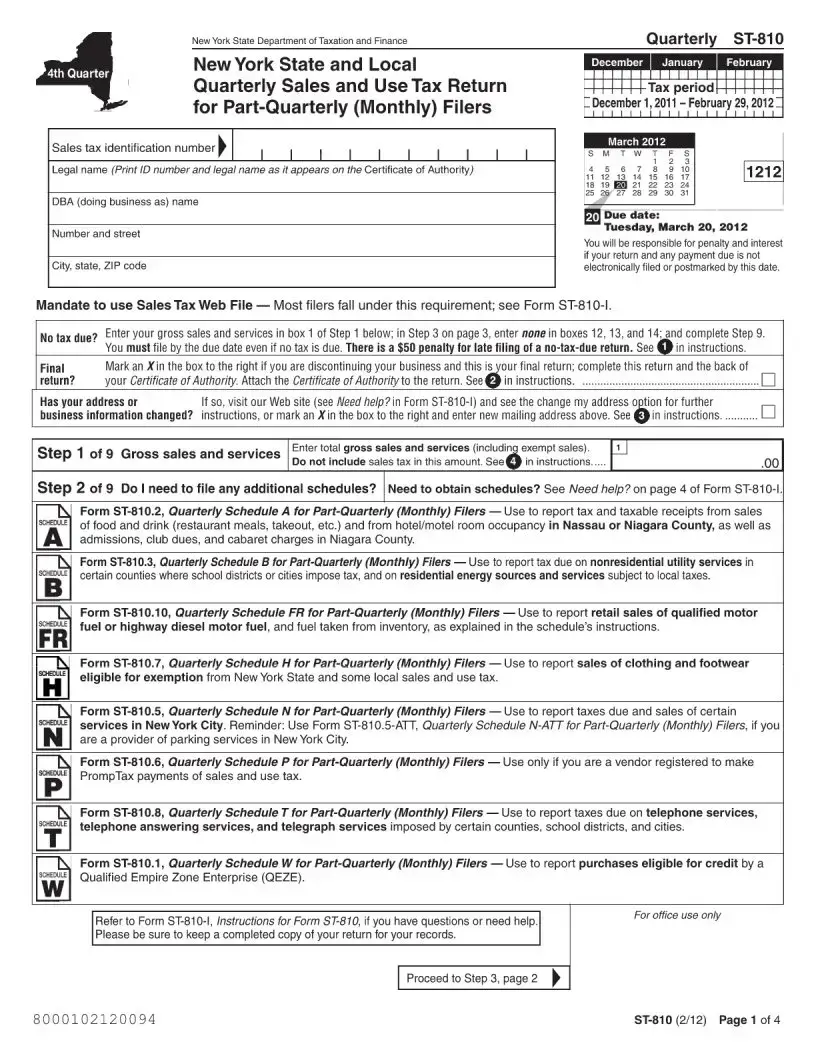

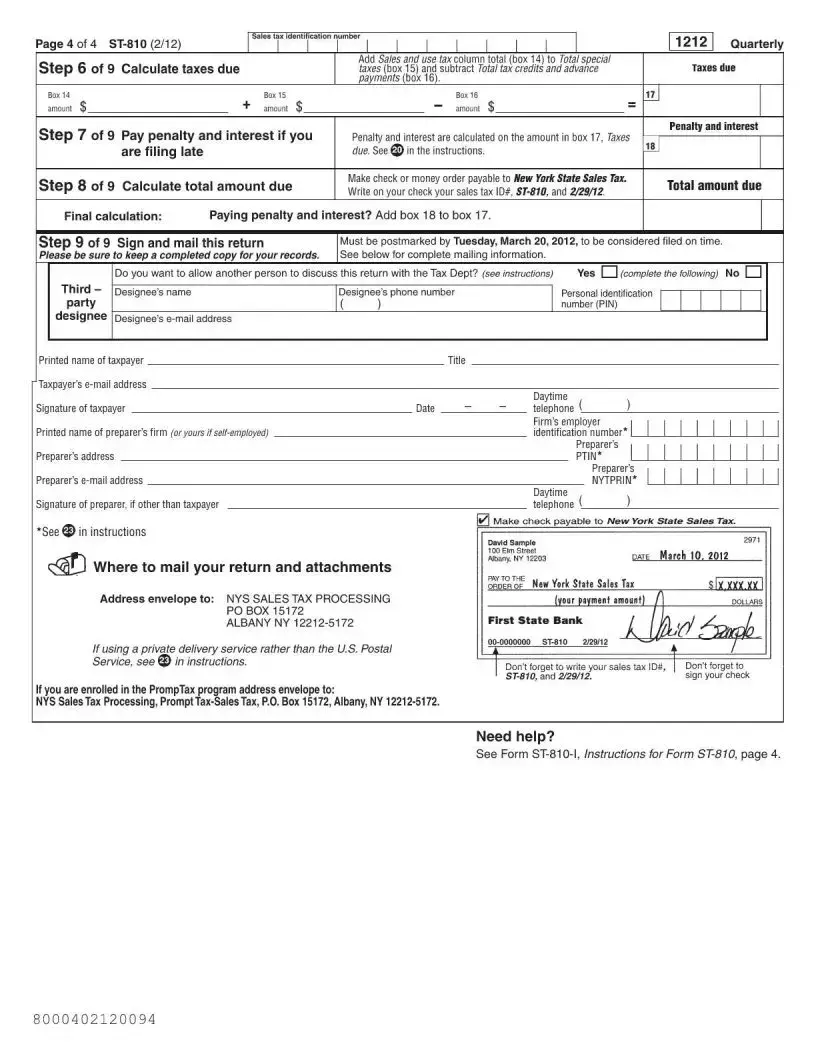

The New York State Department of Taxation and Finance requires businesses to file the ST-810 form, a crucial document for reporting quarterly sales and use taxes. This form is specifically designed for part-quarterly (monthly) filers and is due on the 20th of the month following the end of each quarter. For example, the deadline for the December to February quarter is March 20. Businesses must include their sales tax identification number and legal name as it appears on their Certificate of Authority. Even if no tax is due, filing is mandatory to avoid penalties. The ST-810 form consists of several steps, beginning with the reporting of gross sales and services, and may require additional schedules for specific types of sales, such as food, utilities, or clothing. Each schedule serves a distinct purpose, allowing businesses to report taxes due on various categories of sales and services. Completing the ST-810 accurately is essential, as errors or late submissions can lead to financial penalties and interest charges. Understanding the requirements of this form can help businesses remain compliant and avoid unnecessary complications.

Form ST-810.2, Quarterly Schedule A: This document is used to report tax and taxable receipts specifically from sales of food and drink, as well as hotel room occupancy in certain counties. Like the ST-810 form, it is part of the quarterly reporting process for sales and use tax, ensuring that specific categories of sales are accurately tracked and reported.

Form ST-810.3, Quarterly Schedule B: This schedule focuses on reporting tax due on nonresidential utility services and residential energy sources. Similar to the ST-810, it requires detailed reporting for specific tax categories, maintaining compliance with local tax regulations.

Form ST-810.5, Quarterly Schedule N: This form is designed for reporting taxes due on certain services provided in New York City. It parallels the ST-810 in that both forms require filers to report specific types of sales or services, ensuring that all taxable activities are accounted for.

Form ST-810.10, Quarterly Schedule FR: This schedule is utilized for reporting retail sales of qualified motor fuel. Like the ST-810, it is part of the broader framework for sales tax reporting, ensuring that specific industries are properly taxed and compliant with state regulations.

Filling out the New York ST-810 form can be a straightforward process, but there are common mistakes that individuals and businesses often make. One significant error is failing to include the correct sales tax identification number. This number is essential for processing the return accurately. If this number is missing or incorrect, it can lead to delays or penalties.

Another frequent mistake is neglecting to report all gross sales and services. It is crucial to enter the total gross sales accurately in the designated box. Omitting certain sales, whether they are exempt or not, can result in discrepancies and potential audits.

Many filers also overlook the importance of marking the correct box if they are discontinuing their business. If this is the final return, it is vital to indicate that clearly. Failure to do so can complicate future filings and may lead to unnecessary penalties.

Address changes are often a source of confusion. When a business's address or information changes, it is important to update this on the form. Many individuals forget to mark the box indicating a change, which can lead to miscommunication and delays in receiving important documents from the tax department.

In addition, some filers mistakenly assume that they do not need to file if no tax is due. This is incorrect; even if there is no tax due, the form must still be submitted by the due date to avoid a penalty. A late filing fee of $50 can be incurred for failing to submit a no-tax-due return.

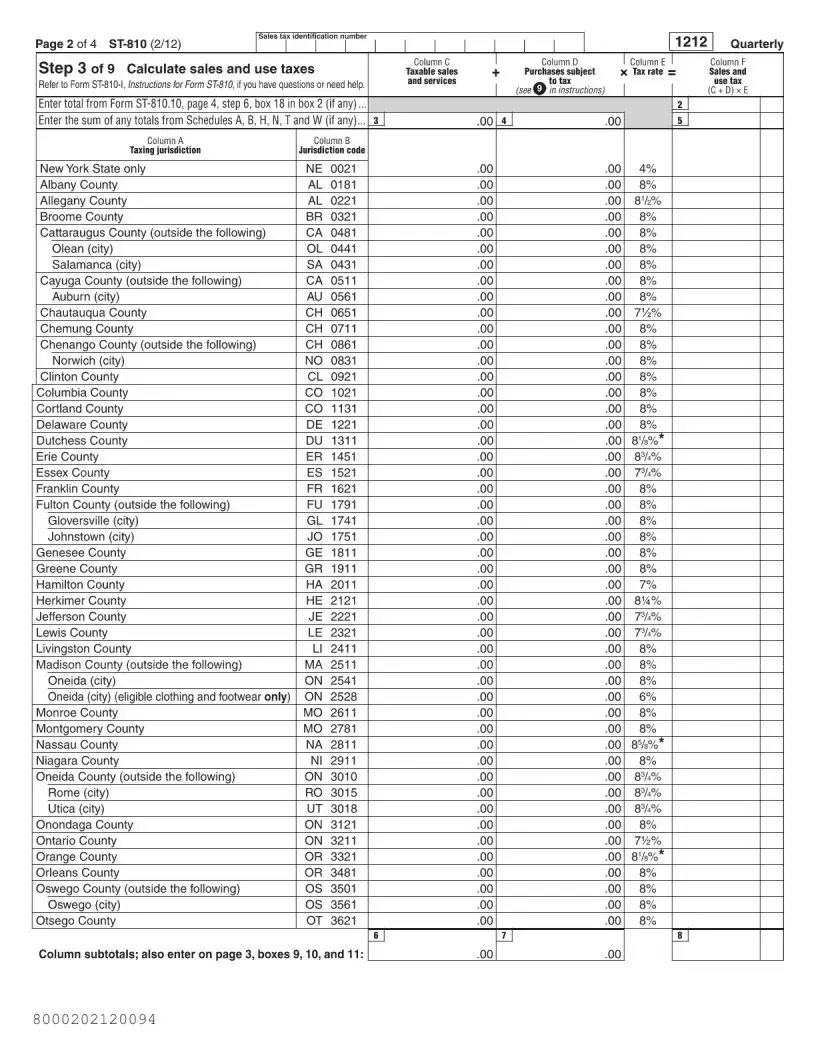

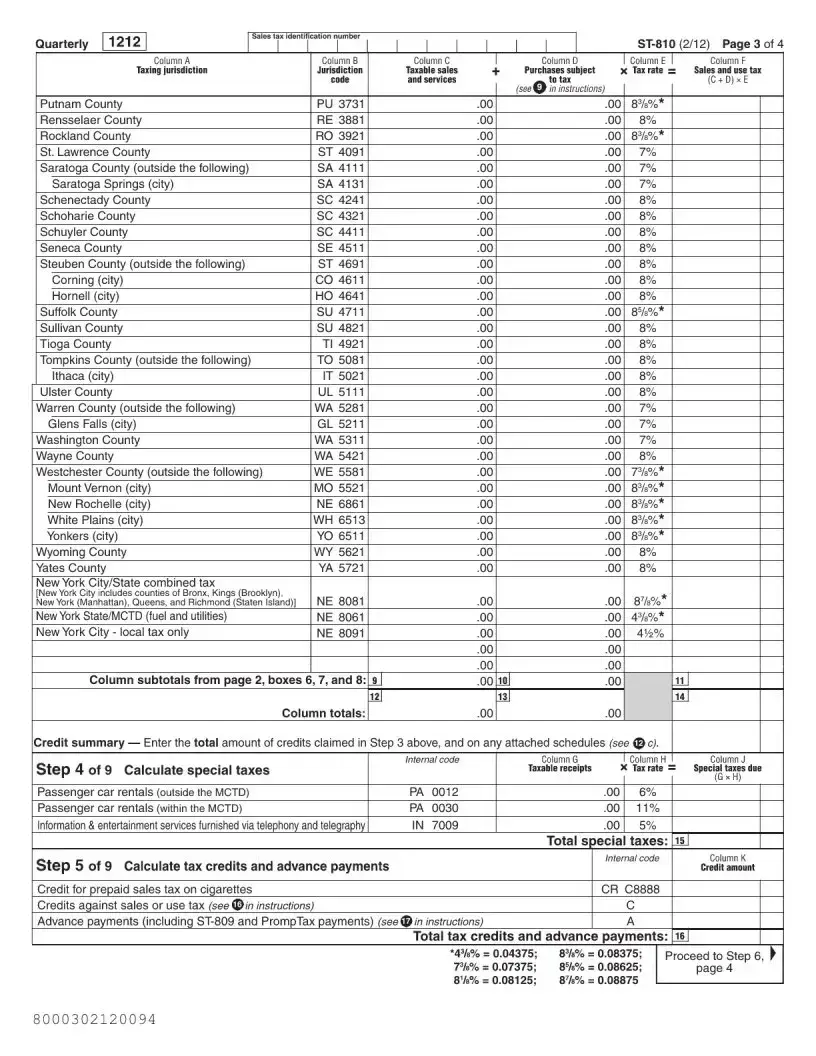

Calculating taxes can also be a source of errors. Some individuals may miscalculate the taxable sales and purchases. It is essential to follow the instructions carefully and ensure that the calculations are accurate. Errors in this area can lead to underpayment or overpayment of taxes.

Another common oversight is neglecting to keep a copy of the completed return. Retaining a copy is important for future reference and can be helpful in case of any discrepancies or audits. Without this documentation, it can be challenging to resolve issues that may arise later.

Additionally, failing to use the appropriate schedules can complicate the filing process. Each schedule serves a specific purpose, and not utilizing them correctly can lead to incomplete information being submitted. Filers should review the instructions to determine which schedules are necessary for their situation.

Lastly, some individuals do not take advantage of the resources available for assistance. The New York State Department of Taxation and Finance provides guidance and help for those who may have questions. Ignoring these resources can lead to avoidable mistakes and complications.

The New York ST-810 form is a quarterly sales and use tax return for businesses that file Part-Quarterly (Monthly). It is used to report sales tax collected and to pay any taxes owed to the state. This form is crucial for compliance with New York State tax regulations.

The ST-810 form is due on the 20th of the month following the end of the quarter. For example, if you are reporting for December, January, and February, your return must be filed by March 20. Late submissions can result in penalties and interest.

You still need to file the ST-810 form even if you have no tax due. Simply report your gross sales and services in the designated box and indicate “none” in the tax due boxes. Failing to file on time can incur a $50 penalty, even for no-tax-due returns.

If you are discontinuing your business, mark the appropriate box on the form. You must complete the return and attach your Certificate of Authority. This ensures that your tax obligations are settled properly.

If your address or business information has changed, you can update it directly on the form. Mark the box indicating a change and enter your new mailing address. For more detailed instructions, visit the New York State Department of Taxation and Finance website.

Depending on your business activities, you may need to file additional schedules. For example, Schedule A is for reporting sales of food and drink, while Schedule N is for certain services in New York City. Refer to the instructions on Form ST-810 for a complete list of required schedules.

Understanding the New York ST-810 form is crucial for compliance with state tax regulations. However, several misconceptions often lead to confusion among filers. Below are nine common misconceptions about the ST-810 form, along with clarifications for each.

Addressing these misconceptions promptly is vital to ensure compliance and avoid unnecessary penalties. Filers should review the instructions carefully and seek assistance if needed.

Nycers Retirement - Make address changes a priority to ensure uninterrupted benefits.

Unincorporated Business Tax - The instructions detail the exemptions allowable when estimating taxes due.

Here are some important points to remember when filling out and using the New York ST-810 form:

Completing the New York ST-810 form involves providing accurate information about your sales and use tax for the specified quarter. After filling out the form, ensure you submit it by the due date to avoid penalties. Follow these steps to complete the form correctly.