Free Ga 4 New York Form

Free Ga 4 New York Form

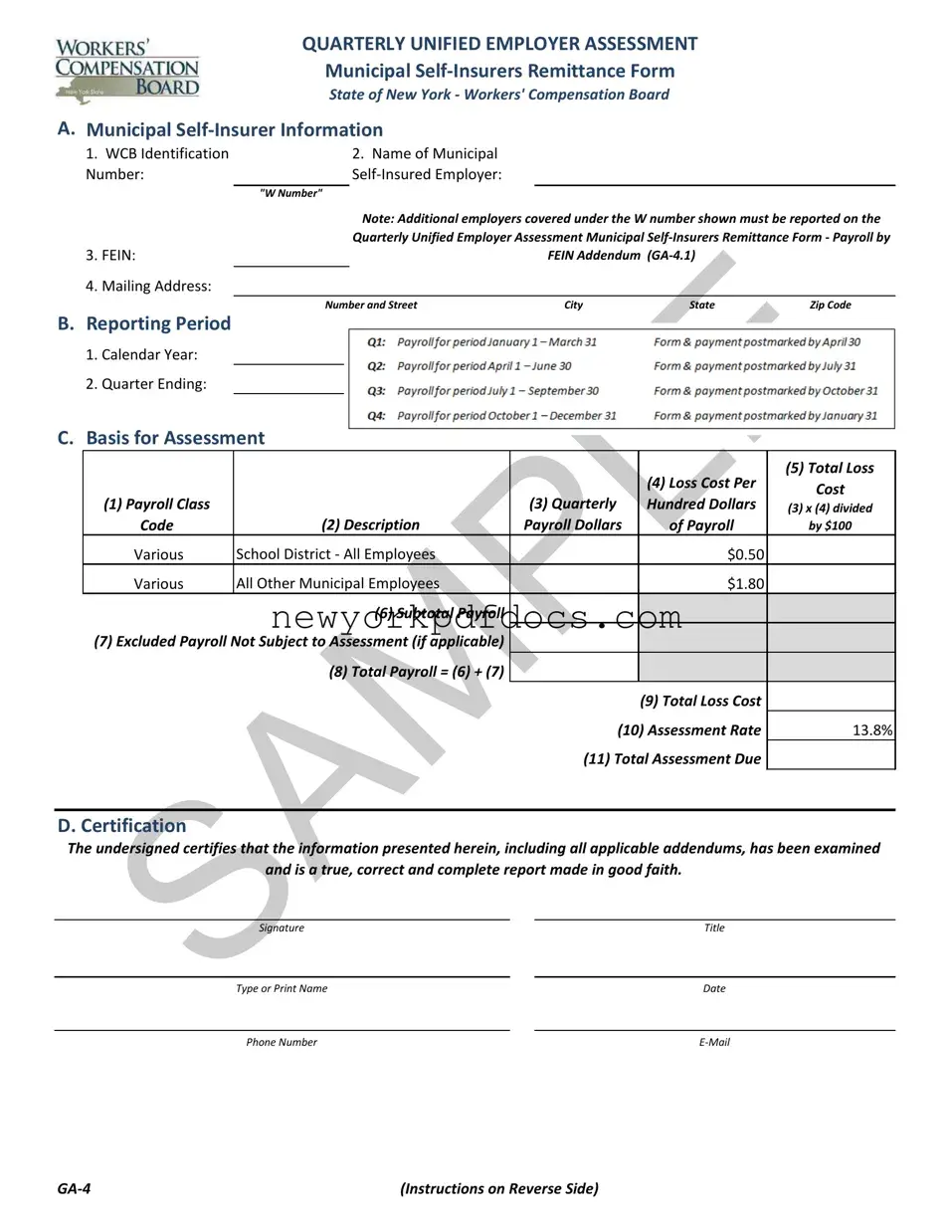

The Quarterly Unified Employer Assessment Municipal Self-Insurers Remittance Form, commonly referred to as the GA-4, serves as a crucial tool for municipal self-insured employers in New York. This form must be completed and submitted each quarter, ensuring compliance with the state's workers' compensation regulations. Key components include essential information about the municipal self-insurer, such as the WCB Identification Number, the legal name of the employer, and the Federal Employer Identification Number (FEIN). The form also requires details about the reporting period, including the calendar year and quarter ending. Employers must calculate their total payroll, which is divided into categories for school districts and other municipal employees, along with the applicable loss costs per hundred dollars of payroll. The total assessment due is then determined by applying a specific assessment rate to the calculated loss costs. Additionally, the form mandates a certification section where the employer attests to the accuracy and completeness of the information provided. Failure to comply with these requirements can lead to significant penalties, including interest on underpayments and potential revocation of self-insured status. Thus, understanding and accurately completing the GA-4 is essential for municipal employers to maintain their self-insured status and avoid legal repercussions.

Form 941: This is the Employer's Quarterly Federal Tax Return. Like the GA-4, it requires employers to report wages paid and taxes withheld. Both forms are submitted quarterly and involve payroll calculations.

NYS-45: The Quarterly Combined Withholding, Wage Reporting, and Unemployment Insurance Return is similar in that it requires reporting of payroll information. Employers must reconcile their payroll figures between the NYS-45 and the GA-4 to ensure accuracy.

Form 940: This is the Employer's Annual Federal Unemployment (FUTA) Tax Return. While it is an annual form, it shares the purpose of reporting payroll information and calculating taxes owed, akin to the quarterly assessments in the GA-4.

W-2 Forms: These are issued to employees and report annual wages and taxes withheld. Both the W-2 and GA-4 involve payroll data but serve different purposes—one for employee reporting and the other for employer assessment.

Form 1099-MISC: This form is used to report payments made to non-employees. Similar to the GA-4, it requires accurate reporting of payments, though it focuses on independent contractors rather than employees.

Form 1096: This is a summary form for information returns, including 1099s. Like the GA-4, it summarizes payroll-related information but is used for reporting to the IRS rather than for state assessments.

State Unemployment Insurance (SUI) Reports: These reports, similar to the GA-4, require employers to report payroll information to state agencies for unemployment insurance purposes, ensuring compliance with state laws.

Workers' Compensation Insurance Reports: These reports are required by insurance carriers to assess risks and premiums. They share the common goal of ensuring proper reporting of payroll and associated costs, like the GA-4.

Payroll Tax Returns: These returns are filed to report payroll taxes withheld from employees. Both the payroll tax returns and the GA-4 involve calculations based on payroll figures and are essential for compliance.

QUARTERLY UNIFIED EMPLOYER ASSESSMENT

Municipal

State of New York - Workers' Compensation Board

A. Municipal

1. |

WCB Identification |

|

2. Name of Municipal |

|

|

|

Number: |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

"W Number" |

|

|

|

|

|

|

|

Note: Additional employers covered under the W number shown must be reported on the |

|||

|

|

|

Quarterly Unified Employer Assessment Municipal |

|||

3. |

FEIN: |

|

|

FEIN Addendum |

|

|

4. |

Mailing Address: |

|

|

|

|

|

|

|

|

|

|

||

|

|

Number and Street |

City |

State |

Zip Code |

|

B.Reporting Period

1.Calendar Year:

2.Quarter Ending:

C.Basis for Assessment

|

|

|

|

(5) Total Loss |

|

|

|

(4) Loss Cost Per |

Cost |

|

|

(3) Quarterly |

|

|

(1) Payroll Class |

|

Hundred Dollars |

(3) x (4) divided |

|

Code |

(2) Description |

Payroll Dollars |

of Payroll |

by $100 |

Various |

School District - All Employees |

|

$0.50 |

|

Various |

All Other Municipal Employees |

|

$1.80 |

|

|

(6) Subtotal Payroll |

$0 |

|

|

(7) Excluded Payroll Not Subject to Assessment (if applicable) |

|

|

|

|

|

(8) Total Payroll = (6) + (7) |

$0 |

|

|

|

|

|

(9) Total Loss Cost |

|

|

|

(10) Assessment Rate |

13.8% |

|

|

|

(11) Total Assessment Due |

|

|

|

|

|

|

|

D. Certification

The undersigned certifies that the information presented herein, including all applicable addendums, has been examined

and is a true, correct and complete report made in good faith.

Signature |

|

Title |

|

|

|

Type or Print Name |

|

Date |

|

|

|

Phone Number |

|

(Instructions on Reverse Side) |

Instructions for Completing Quarterly Unified Employer Assessment

Municipal

General Instructions

1.The Quarterly Unified Employer Assessment Municipal

2.Additional municipal employers covered under the W number shown must be reported on the Quarterly Unified Employer Assessment Municipal Self- Insurers Remittance Form - Payroll by FEIN Addendum

3.Questions about the form or process should be directed to WCBFinanceOffice@wcb.ny.gov.

4.Checks are to be made payable to the Chair, NYS Workers' Compensation Board.

5.To ensure the proper application of payment please include W Number and applicable quarter on check.

6.This report and corresponding payment, along with applicable addendum, must be submitted quarterly by every municipal employer actively self- insured for workers' compensation. Employers that discontinued their

Submit completed form via

WCBFinanceOffice@wcb.ny.gov

and mail check to address below

Or mail completed form and check to:

New York State Workers’ Compensation Board

328 State Street

Finance Unit, Room 331

Schenectady, NY

Municipal

1.The WCB Identification Number or "W Number" as assigned to the municipal

2.The Name of the Municipal

3.The FEIN, or Federal Employer Identification Number, must be reported for the municipal

4.The full mailing address of the municipal

Basis for Assessment

1.A blended rate for municipal payroll will be used and there is no need to breakout by class.

2.Payroll must be broken out between employers which are school districts and all other municipal employers.

3.Total quarterly payroll associated with either the school district and/or all other types of municipal

4.The loss cost per hundred dollars of payroll for municipal employers and school districts is set annually by the Chair. The rates are shown on the Quarterly Unified Employer Assessment Municipal

5.The total loss cost is determined by multiplying the payroll by the loss cost shown and dividing by $100.

6.Subtotal of payroll reported on the Quarterly Unified Employer Assessment Municipal

7.Excluded payroll not subject to assessment.

8.With limited exception, total payroll should agree with that reported on the Quarterly Combined Withholding, Wage Reporting and Unemployment

|

Insurance Return |

|

please provide reconciliation. No payroll caps are to be applied. |

9. |

Equal to the sum of all of the loss cost by payroll class shown. |

10. |

The assessment rate for the rating period established by the Chair pursuant to WCL Section 151. This can be found on the WCB's website |

|

www.wcb.ny.gov. |

11. |

The total assessment due is equal to the total loss cost multipled by the assessment rate. |

Certification

In accordance with WCL Section 151 the Chair may conduct periodic audits of any

QUARTERLY UNIFIED EMPLOYER ASSESSMENT

Municipal

Payroll by FEIN Addendum

State of New York - Workers' Compensation Board

A. Municipal

|

|

2. Name of |

1. WCB Identification |

|

Municipal Self- |

Number: |

|

Insured Employer: |

|

|

|

|

"W Number" |

|

B.Reporting Period

1.Calendar Year:

2.Quarter Ending:

C.Municipal Employers Covered Under the W Number Shown Above

|

|

|

(4) Excluded |

|

|

(3) Quarterly |

Payroll (if |

(1) FEIN |

(2) Municipal |

Payroll |

applicable) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(5) Subtotal Payroll |

|

|

|

(6) Subtotal Excluded Payroll (if applicable) |

|

|

|

(7) Total Payroll = (5) + (6) |

|

$0 |

|

|

|

|

Instructions for Completing Quarterly Unified Employer Assessment

Municipal

Payroll by FEIN Addendum

General Instructions

1.The Quarterly Unified Employer Assessment Municipal

2.The Quarterly Unified Employer Assessment Municipal

3.The payroll by class code reported on the Quarterly Unified Employer Assessment Municipal

4.Questions about the form or process should be directed to WCBFinanceOffice@wcb.ny.gov.

5.This addendum, if applicable, must be sent quarterly with the Quarterly Unified Employer Assessment Municipal

Municipal

1.The WCB Identification Number or "W number" as assigned to the municipal

2.The Name of the Municipal

Municipal Employers Covered Under the W Number

1.The FEIN, or Federal Employer Identification Number, must be reported for the municipal

2.The municipal

3.Total quarterly payroll associated with the FEIN number.

4.Excluded payroll not subject to assessment.

5.Subtotal of payroll subject to assessment of the Quarterly Unified Employer Assessment Municipal

6.Subtotal of excluded payroll not subject to the assessment of the Quarterly Unified Employer Assessment Municipal

7.Total payroll and excluded payroll if applicable. With limited exception, total payroll should agree with that reported on the Quarterly Combined

Withholding, Wage Reporting and Unemployment Insurance Return

Filling out the GA-4 New York form can be a straightforward process, but there are common mistakes that people often make. One mistake is failing to include the correct WCB Identification Number, also known as the "W Number." This number is essential as it identifies the municipal self-insurer. Omitting or incorrectly entering this number can lead to delays or issues with processing the form.

Another frequent error involves the name of the municipal self-insured employer. It is crucial to use the full legal name as approved for self-insurance. Abbreviations or informal names can result in confusion and may lead to complications in the assessment process.

Many individuals also overlook the importance of providing the correct Federal Employer Identification Number (FEIN). This number must be reported accurately for the municipal self-insurer. If there are additional employers under the same W number, they must also be reported using the appropriate addendum. Failing to do so can result in incomplete information being submitted.

Additionally, errors in reporting the mailing address are common. The address provided should be complete and accurate, as it will be used for all correspondence related to the assessment. Incomplete addresses can lead to missed communications and potential issues with compliance.

Another mistake occurs in the calculation of payroll figures. It is important to break down payroll correctly between school districts and other municipal employers. Not doing this can lead to incorrect assessments and potential penalties. Furthermore, individuals sometimes forget to include excluded payroll not subject to assessment, which should be clearly indicated on the form.

People often miscalculate the total payroll as well. The total payroll should align with the figures reported on the Quarterly Combined Withholding, Wage Reporting, and Unemployment Insurance Return (NYS-45). If discrepancies exist, a reconciliation should be provided. Ignoring this can result in penalties or audits.

Another common oversight is not including the assessment rate or miscalculating the total assessment due. The assessment rate is set annually, and failing to apply it correctly can lead to underpayment or overpayment, both of which can have financial implications.

Lastly, individuals sometimes neglect the certification section of the form. The certification must be signed and dated by an authorized individual. Incomplete certifications can render the form invalid and lead to further complications in the assessment process.

What is the GA-4 New York form?

The GA-4 form, officially known as the Quarterly Unified Employer Assessment Municipal Self-Insurers Remittance Form, is a document that must be completed by active municipal self-insured employers in New York. It is used to report payroll information and calculate the assessment due for workers' compensation purposes.

Who needs to submit the GA-4 form?

Every active municipal self-insured employer is required to submit the GA-4 form. Employers that have discontinued their self-insurance program or those that are actively or inactively self-insured for disability benefits do not need to submit this form.

When is the GA-4 form due?

The GA-4 form must be submitted quarterly, within thirty days after the end of each quarter. This ensures timely reporting and payment of the assessment due.

What information is required on the GA-4 form?

The form requires the following information:

How is the assessment calculated?

The assessment is calculated based on total payroll and the applicable loss cost per hundred dollars of payroll. The total loss cost is determined by multiplying the payroll by the loss cost rate and dividing by 100. The final assessment due is calculated by multiplying the total loss cost by the assessment rate, which is currently set at 13.8%.

What should be done if there are additional employers under the same W number?

If there are additional municipal employers covered under the same W number, they must be reported using the Payroll by FEIN Addendum (GA-4.1). This addendum must be submitted along with the GA-4 form.

What are the consequences of inaccurate reporting?

If a self-insurer underpays an assessment due to inaccurate reporting, they will be responsible for paying the full amount of the underpaid assessment along with interest. In cases of material misrepresentation, additional penalties may apply, including a possible class E felony charge.

How should the GA-4 form and payment be submitted?

The completed GA-4 form should be submitted via email to WCBFinanceOffice@wcb.ny.gov. Payment should be mailed to the New York State Workers’ Compensation Board, along with the completed form. Checks should be made payable to the Chair, NYS Workers' Compensation Board, and must include the W number and applicable quarter on the check.

Understanding the GA-4 New York form can be challenging due to several misconceptions. Here are seven common misunderstandings along with clarifications:

By addressing these misconceptions, municipal self-insured employers can ensure accurate reporting and compliance with the requirements set forth by the New York State Workers' Compensation Board.

How Long Can an Insurance Claim Stay Open - Keep accurate records to support the details provided on the NF-7 form.

Nys Nbs - Applicants must possess a valid New York State license for taking big game.

Filling out the GA-4 New York form requires careful attention to detail. Here are some key takeaways to help you navigate the process effectively:

By following these key points, you can ensure that your GA-4 form is completed accurately and submitted on time, helping you maintain compliance with New York's regulations.

Completing the GA-4 form is essential for municipal self-insurers in New York. This form must be filled out accurately to ensure compliance with state regulations. Follow these steps to complete the form correctly.

After completing the GA-4 form, ensure that it is submitted along with the required payment within thirty days of the quarter's end. For any questions, reach out to the provided contact email. Proper submission will help maintain compliance and avoid penalties.