Valid Deed in Lieu of Foreclosure Document for New York

Valid Deed in Lieu of Foreclosure Document for New York

In the landscape of real estate transactions, the New York Deed in Lieu of Foreclosure form serves as a critical tool for homeowners facing financial difficulties. This legal document allows a homeowner to voluntarily transfer ownership of their property to the lender, thereby avoiding the lengthy and often stressful foreclosure process. By executing this form, the homeowner can mitigate the negative impacts of foreclosure on their credit score and potentially negotiate more favorable terms regarding any remaining mortgage debt. The form outlines key components such as the identification of the parties involved, a clear description of the property, and the specific terms under which the deed is transferred. Additionally, it may include provisions that protect the homeowner from future liability on the mortgage, depending on the agreement reached with the lender. Understanding the nuances of this form is essential for both homeowners and lenders, as it can facilitate a smoother transition and provide a pathway to financial recovery.

The Deed in Lieu of Foreclosure form is an important legal document that allows a homeowner to transfer ownership of their property to the lender to avoid foreclosure. Several other documents serve similar purposes in the realm of real estate and financial transactions. Here’s a list of seven documents that share similarities with the Deed in Lieu of Foreclosure:

Understanding these documents can empower homeowners facing financial difficulties. Each offers a unique approach to addressing mortgage challenges and can help avoid the severe consequences of foreclosure.

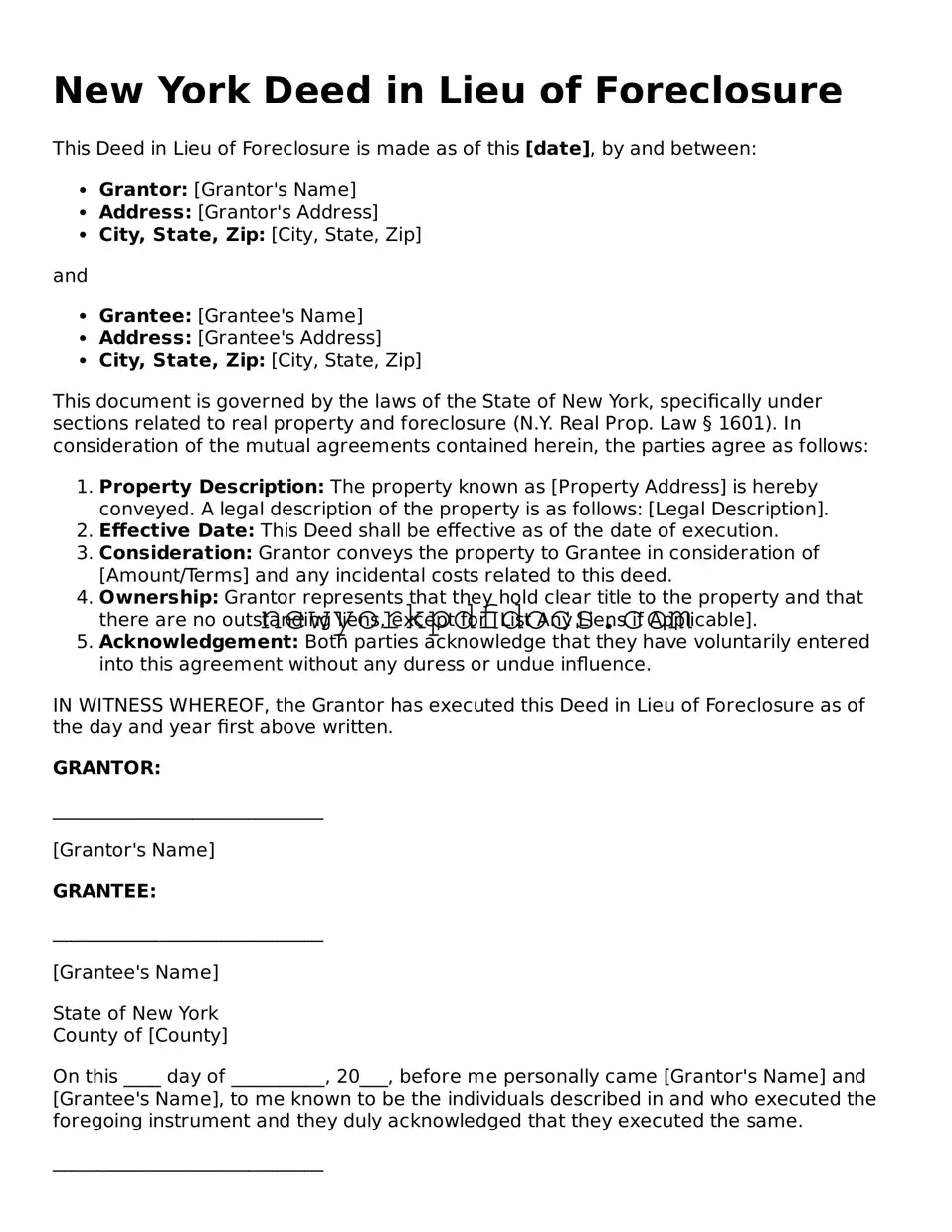

New York Deed in Lieu of Foreclosure

This Deed in Lieu of Foreclosure is made as of this [date], by and between:

and

This document is governed by the laws of the State of New York, specifically under sections related to real property and foreclosure (N.Y. Real Prop. Law § 1601). In consideration of the mutual agreements contained herein, the parties agree as follows:

IN WITNESS WHEREOF, the Grantor has executed this Deed in Lieu of Foreclosure as of the day and year first above written.

GRANTOR:

_____________________________

[Grantor's Name]

GRANTEE:

_____________________________

[Grantee's Name]

State of New York

County of [County]

On this ____ day of __________, 20___, before me personally came [Grantor's Name] and [Grantee's Name], to me known to be the individuals described in and who executed the foregoing instrument and they duly acknowledged that they executed the same.

_____________________________

Notary Public

Filling out a Deed in Lieu of Foreclosure form in New York can be a complex process. Many individuals make mistakes that can lead to delays or complications in the transfer of property. Understanding common pitfalls can help homeowners navigate this process more smoothly.

One frequent mistake is failing to include all necessary parties in the form. The deed must list not only the current property owner but also any co-owners or lienholders. Omitting a co-owner can lead to legal disputes down the line, as their rights may not be acknowledged in the transfer. It is essential to ensure that everyone who has a legal interest in the property is included.

Another common error is neglecting to provide accurate property descriptions. The deed must contain a precise legal description of the property, which typically includes the lot number and any relevant boundaries. If this information is incorrect or incomplete, it could create issues with the validity of the deed and may complicate future transactions.

People often overlook the importance of notarization. A Deed in Lieu of Foreclosure must be signed in front of a notary public to be considered valid. Failing to have the document notarized can result in the deed being rejected by the lender, which would negate the entire process.

Additionally, some individuals do not fully understand the implications of the deed. A Deed in Lieu of Foreclosure transfers ownership of the property to the lender, but it may also have tax consequences. Homeowners should consult with a tax professional to understand how this transfer could affect their financial situation.

Inaccurate dates can also pose a problem. The form requires the date of execution, and if this date is incorrect or missing, it could lead to confusion regarding the timeline of the transaction. It is crucial to double-check all dates before submitting the form.

Another mistake is not including a statement of consideration. This section outlines what the lender will receive in exchange for accepting the deed. Without this information, the lender may question the validity of the transaction, potentially leading to delays.

Many people also fail to read the fine print. The Deed in Lieu of Foreclosure form may contain specific clauses or requirements that need to be understood before signing. Ignoring these details can lead to unexpected obligations or limitations on the homeowner's rights.

Finally, individuals sometimes rush the process without seeking professional advice. Consulting with a real estate attorney or a qualified professional can provide valuable insights and help avoid common mistakes. Taking the time to understand the form and its implications can lead to a smoother transition and a more favorable outcome.

A Deed in Lieu of Foreclosure is a legal document that allows a homeowner to voluntarily transfer ownership of their property to the lender in order to avoid foreclosure. This process can help the homeowner to mitigate the negative impacts of foreclosure on their credit score and may allow them to walk away from the mortgage obligation.

Typically, homeowners who are facing financial difficulties and are unable to continue making mortgage payments may qualify. Lenders usually require that the borrower is in default or at risk of defaulting on their loan. Additionally, the property must be free of any liens or other encumbrances, which means that the homeowner should not have other outstanding debts tied to the property.

There are several benefits to consider. First, it can be less damaging to a homeowner's credit score compared to a foreclosure. Second, the process is often quicker and less expensive than going through a full foreclosure. Finally, homeowners may be able to negotiate terms with the lender, such as potential relocation assistance or forgiveness of remaining debt.

While a Deed in Lieu of Foreclosure can be beneficial, there are also downsides. Homeowners may have to pay taxes on any forgiven debt, as it can be considered taxable income. Additionally, lenders may not always agree to this option, and homeowners may still face challenges in negotiating favorable terms.

The process typically begins with the homeowner contacting their lender to express interest in a Deed in Lieu of Foreclosure. The lender will then evaluate the homeowner's financial situation and the property's condition. If approved, both parties will sign the deed, transferring ownership to the lender. The lender may also require the homeowner to vacate the property by a certain date.

While it is not strictly necessary to have legal assistance, it is highly recommended. An attorney can help navigate the complexities of the agreement, ensuring that the homeowner understands their rights and obligations. They can also assist in negotiating terms with the lender.

Yes, a Deed in Lieu of Foreclosure will impact your credit score, but generally less severely than a foreclosure. The exact effect can vary based on your overall credit history and the scoring model used. It is advisable to check your credit report after the process is completed to understand its impact.

Yes, it is possible to obtain a mortgage after a Deed in Lieu of Foreclosure, but it may take some time. Lenders typically require a waiting period, which can range from two to four years, depending on the lender and the specific circumstances. Rebuilding your credit during this time can improve your chances of securing a new mortgage.

Understanding the New York Deed in Lieu of Foreclosure can be challenging. Here are ten common misconceptions about this process, along with clarifications to help demystify it.

A Deed in Lieu of Foreclosure transfers ownership of the property to the lender, but it does not automatically erase all debts. Homeowners may still be responsible for other financial obligations, such as second mortgages or personal loans secured by the property.

While it may seem like a straightforward option, the process can be lengthy. Lenders often require extensive documentation and may take time to review the homeowner's financial situation before accepting a Deed in Lieu.

Once the deed is transferred to the lender, the homeowner relinquishes all rights to the property. This means they will no longer have ownership or the ability to live in the home.

Although both result in the loss of the home, a Deed in Lieu is a voluntary agreement between the homeowner and the lender. Foreclosure is a legal process initiated by the lender, often resulting in more significant financial and credit consequences for the homeowner.

A Deed in Lieu of Foreclosure requires the lender's consent. Homeowners must negotiate with their lender and follow specific procedures to complete the transfer.

While a Deed in Lieu may be less damaging than a foreclosure, it can still negatively impact the homeowner's credit score. The extent of this impact varies based on individual circumstances and credit history.

Not every homeowner qualifies for a Deed in Lieu of Foreclosure. Lenders typically evaluate the homeowner's financial situation, the property's value, and other factors before approving this option.

Homeowners may still face legal consequences or tax implications following the transfer of the deed. It is essential to understand the potential liabilities that may arise even after the deed is signed.

A Deed in Lieu of Foreclosure may resolve the immediate issue of homeownership, but it does not address underlying financial difficulties. Homeowners should consider seeking financial counseling to prevent future issues.

While it may provide relief from mortgage payments, a Deed in Lieu does not guarantee a fresh start. Homeowners may still face challenges in securing new housing or rebuilding their financial stability.

Nys Division of Corporations - The articles may dictate the distribution of profits among shareholders.

Free Firearm Bill of Sale - Helps maintain a record of firearm transactions for future reference.

Filling out and using the New York Deed in Lieu of Foreclosure form can be a crucial step for homeowners facing foreclosure. Here are some key takeaways to consider:

By following these guidelines, homeowners can navigate the process of using a Deed in Lieu of Foreclosure more effectively and with greater confidence.

Once you have the New York Deed in Lieu of Foreclosure form ready, it is important to complete it accurately to ensure a smooth process. After filling out the form, you will need to submit it to the appropriate parties involved in the foreclosure process. This typically includes your lender and may require additional documentation.