Free Char500 Nys Form

Free Char500 Nys Form

The CHAR500 form is an essential document for charitable organizations operating in New York State, serving as their annual filing for compliance with state regulations. This form collects crucial information about the organization, including its fiscal year, contact details, and registration category—whether it falls under 7A, EPTL, DUAL, or is exempt. Organizations must also certify the accuracy of their submitted information, ensuring transparency and accountability. Depending on their financial activities, organizations may qualify for exemptions that simplify their filing process, allowing them to submit only the CHAR500 without additional schedules or fees. If they do not meet these exemptions, they will need to provide detailed financial reports and pay applicable fees based on their revenue and asset levels. The form also includes specific sections for organizations that have engaged professional fundraisers or received government grants, requiring them to disclose relevant details. By understanding and properly completing the CHAR500, organizations can maintain their good standing and continue their vital work in the community.

IRS Form 990: Like the CHAR500, this form is used by tax-exempt organizations to report their financial information to the IRS. Both documents require organizations to disclose revenue, expenses, and other financial details.

IRS Form 990-EZ: This is a shorter version of Form 990 for smaller organizations. Similar to the CHAR500, it simplifies the reporting process for organizations with less complex financials.

IRS Form 990-PF: Private foundations use this form to report their financial activities. Both the CHAR500 and Form 990-PF require detailed financial disclosures and compliance with state and federal regulations.

IRS Form 990-N (e-Postcard): Smaller nonprofits can use this simplified form to report their income. Like the CHAR500, it serves to inform authorities about the organization's status and activities, although it requires less detail.

California Form RRF-1: This is California's annual registration renewal form for charitable organizations. Similar to the CHAR500, it ensures compliance with state laws and requires annual financial disclosures.

Florida Form DR-1: Charitable organizations in Florida must file this form to register and report their activities. Like the CHAR500, it helps maintain transparency and accountability in charitable operations.

Texas Form 990: In Texas, nonprofits must file this form, which is similar to the CHAR500 in that it collects vital information about the organization’s finances and operations.

Michigan Form 1023: This form is used for obtaining tax-exempt status in Michigan. It shares similarities with the CHAR500 in that both require detailed information about the organization’s purpose and financials.

New Jersey Form CRI-200: This form is required for charitable organizations in New Jersey to register and report their financial activities. It serves a similar purpose as the CHAR500 in ensuring compliance with state regulations.

Ohio Form Charitable Registration: This form is used by charitable organizations in Ohio for registration and annual reporting. Like the CHAR500, it aims to promote transparency and accountability in charitable fundraising.

CHAR500 |

NYS Office of the Attorney General |

2019 |

|

|

Send with fee and attachments to: |

|

|

NYS Annual Filing for Charitable Organizations |

Charities Bureau Registration Section |

Open to Public |

|

28 Liberty Street |

|||

Inspection |

|||

www.CharitiesNYS.com |

New York, NY 10005 |

||

|

|

|

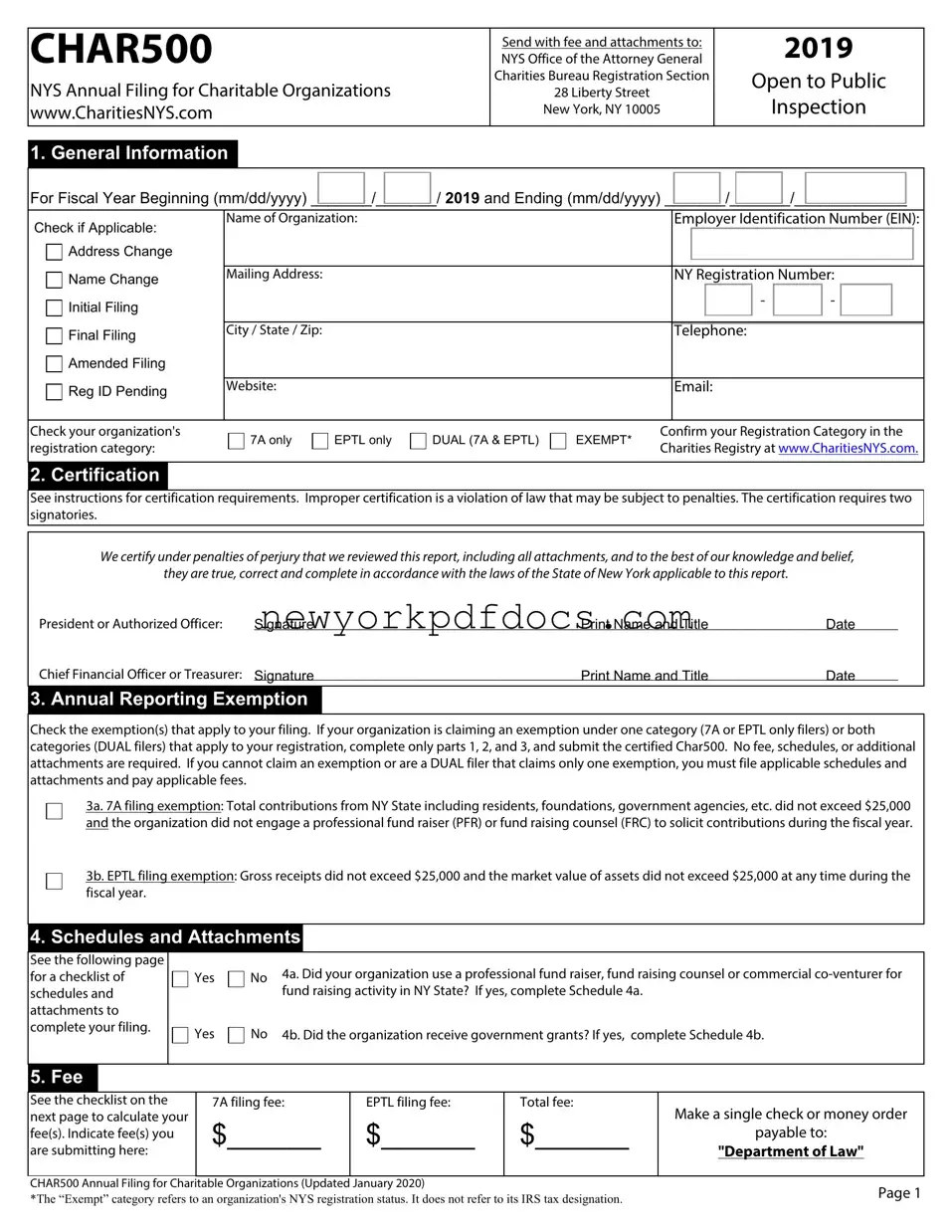

1. General Information

For Fiscal Year Beginning (mm/dd/yyyy) _______/_______/ 2019 and Ending (mm/dd/yyyy) _______/_______/_____________

Check if Applicable:

Address Change

Address Change

Name Change

Name Change

Initial Filing

Initial Filing

Final Filing

Final Filing

Amended Filing

Amended Filing

Reg ID Pending

Reg ID Pending

Name of Organization:

Mailing Address:

City / State / Zip:

Website:

Employer Identification Number (EIN):

NY Registration Number:

- |

|

- |

|

|

|

Telephone:

Email:

Check your organization's |

|

7A only |

|

EPTL only |

|

DUAL (7A & EPTL) |

|

|

|

|

|

||||

registration category: |

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

EXEMPT*

Confirm your Registration Category in the

Charities Registry at www.CharitiesNYS.com.

2. Certification

See instructions for certification requirements. Improper certification is a violation of law that may be subject to penalties. The certification requires two signatories.

We certify under penalties of perjury that we reviewed this report, including all attachments, and to the best of our knowledge and belief,

they are true, correct and complete in accordance with the laws of the State of New York applicable to this report.

President or Authorized Officer: |

Signature |

Print Name and Title |

Date |

Chief Financial Officer or Treasurer: |

Signature |

Print Name and Title |

Date |

3. Annual Reporting Exemption

Check the exemption(s) that apply to your filing. If your organization is claiming an exemption under one category (7A or EPTL only filers) or both categories (DUAL filers) that apply to your registration, complete only parts 1, 2, and 3, and submit the certified Char500. No fee, schedules, or additional attachments are required. If you cannot claim an exemption or are a DUAL filer that claims only one exemption, you must file applicable schedules and attachments and pay applicable fees.

3a. 7A filing exemption: Total contributions from NY State including residents, foundations, government agencies, etc. did not exceed $25,000 and the organization did not engage a professional fund raiser (PFR) or fund raising counsel (FRC) to solicit contributions during the fiscal year.

3b. EPTL filing exemption: Gross receipts did not exceed $25,000 and the market value of assets did not exceed $25,000 at any time during the fiscal year.

4. Schedules and Attachments

See the following page for a checklist of schedules and attachments to complete your filing.

|

Yes |

|

No |

4a. Did your organization use a professional fund raiser, fund raising counsel or commercial |

|

|

|||

|

|

fund raising activity in NY State? If yes, complete Schedule 4a. |

||

|

Yes |

|

No |

|

|

|

4b. Did the organization receive government grants? If yes, complete Schedule 4b. |

||

|

|

5. Fee

See the checklist on the next page to calculate your fee(s). Indicate fee(s) you are submitting here:

7A filing fee:

$______

EPTL filing fee:

$______

Total fee:

$______

Make a single check or money order

payable to:

"Department of Law"

CHAR500 Annual Filing for Charitable Organizations (Updated January 2020) |

Page 1 |

|

*The “Exempt” category refers to an organization's NYS registration status. It does not refer to its IRS tax designation. |

||

|

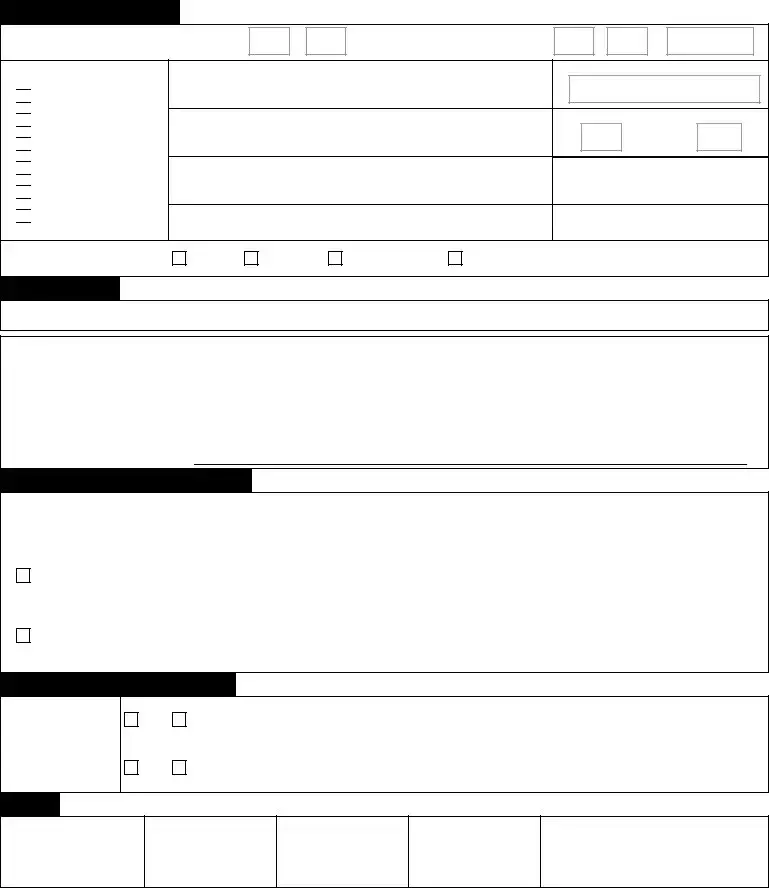

CHAR500

Annual Filing Checklist

Simply submit the certified CHAR500 with no fee, schedule, or additional attachments IF:

-Your organization is registered as 7A only and you marked the 7A filing exemption in Part 3.

-Your organization is registered as EPTL only and you marked the EPTL filing exemption in Part 3.

-Your organization is registered as DUAL and you marked both the 7A and EPTL filing exemption in Part 3.

Checklist of Schedules and Attachments

Check the schedules you must submit with your CHAR500 as described in Part 4:

If you answered "yes" in Part 4a, submit Schedule 4a: Professional Fund Raisers (PFR), Fund Raising Counsel (FRC), Commercial

If you answered "yes" in Part 4b, submit Schedule 4b: Government Grants

Check the financial attachments you must submit with your CHAR500:

IRS Form 990,

All additional IRS Form 990 Schedules, including Schedule B (Schedule of Contributors). Schedule B of public charities is exempt from disclosure and will not be available for public review.

Our organization was eligible for and filed an IRS

If you are a 7A only or DUAL filer, submit the applicable independent Certified Public Accountant's Review or Audit Report:

Review Report if you received total revenue and support greater than $250,000 and up to $750,000.

Audit Report if you received total revenue and support greater than $750,000

No Review Report or Audit Report is required because total revenue and support is less than $250,000

We are a DUAL filer and checked box 3a, no Review Report or Audit Report is required

Calculate Your Fee

For 7A and DUAL filers, calculate the 7A fee:

$0, if you checked the 7A exemption in Part 3a

$25, if you did not check the 7A exemption in Part 3a

For EPTL and DUAL filers, calculate the EPTL fee:

$0, if you checked the EPTL exemption in Part 3b

$25, if the NET WORTH is less than $50,000

$50, if the NET WORTH is $50,000 or more but less than $250,000

$100, if the NET WORTH is $250,000 or more but less than $1,000,000

$250, if the NET WORTH is $1,000,000 or more but less than $10,000,000

$750, if the NET WORTH is $10,000,000 or more but less than $50,000,000

$1500, if the NET WORTH is $50,000,000 or more

Is my Registration Category 7A, EPTL, DUAL or EXEMPT? Organizations are assigned a Registration Category upon registration with the NY Charities Bureau:

7A filers are registered to solicit contributions in New York under Article

EPTL filers are registered under the Estates, Powers & Trusts Law ("EPTL") because they hold assets and/or conduct activites for charitable purposes in NY.

DUAL filers are registered under both 7A and EPTL.

EXEMPT filers have registered with the NY Charities Bureau and meet conditions in Schedule E - Registration Exemption for Charitable Organizations. These organizations are not required to file annual financial reports but may do so voluntarily.

Confirm your Registration Category and learn more about NY law at www.CharitiesNYS.com.

Send Your Filing

Send your CHAR500, all schedules and attachments, and total fee to:

NYS Office of the Attorney General

Charities Bureau Registration Section

28 Liberty Street

New York, NY 10005

Need Assistance?

Visit: www.CharitiesNYS.com

Call: (212)

Email: Charities.Bureau@ag.ny.gov

Where do I find my organization's NET WORTH? NET WORTH for fee purposes is calculated on:

-IRS From 990 Part I, line 22

-IRS Form 990 EZ Part I line 21

-IRS Form 990 PF, calculate the difference between Total Assets at Fair Market Value (Part II, line 16(c)) and Total Liabilities (Part II, line 23(b)).

CHAR500 Annual Filing for Charitable Organizations (Updated January 2020) |

Page 2 |

CHAR500 |

Visit: |

www.CharitiesNYS.com |

2019 |

|

|

Need Assistance? |

|

||

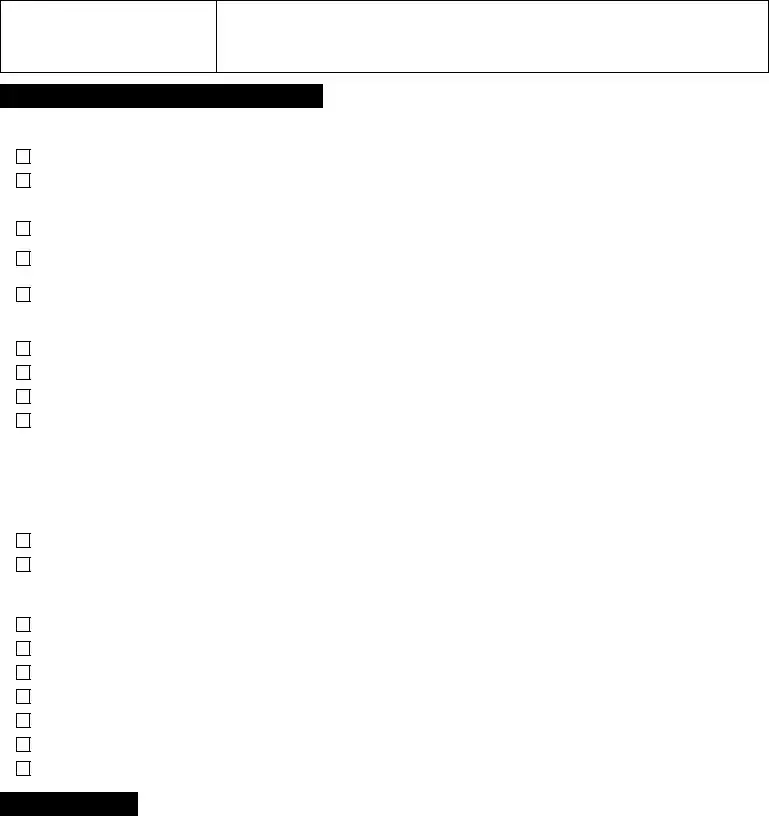

Instructions for Completing Your NY Annual Filing |

Call: |

(212) |

Open to Public |

|

Email: Charities.Bureau@ag.ny.gov |

Inspection |

|||

www.CharitiesNYS.com |

||||

|

|

|||

|

|

|

|

|

Before You Begin

Visit www.CharitiesNYS.com and search the Charities Registry to find your organization's NY State Registration Number

1. General Information

Enter the accounting period covered by the report. Provide the best contact information for your organization. This information will be publicly available in the Charities Registry and will be used for communication to your organization. If your organization is registered and this is your regular annual filing, check Initial Filing. If your contact information needs to be updated, check Address Change and/or Name Change. Check Amended Filing if you are making a change to a previous filing. If you have submitted a CHAR410 - Registration Statement for Charitable Organizations - but do not yet have a NY State Registration Number, check NY Reg Pending. If this is a final filing and the organization is seeking dissolution or ceasing operations, check Final Filing and submit all applicable IRS schedules and attachments. If your organization is a NY corporation, visit www.CharitiesNYS.com for information on how to dissolve. Check the Charities Bureau Registration Category of your organization (7A, EPTL, DUAL, or EXEMPT). EXEMPT organizations are those that have registered with the NY Charities Bureau and meet conditions in Schedule E - Registration Exemption for Charitable Organizations - but have registered and file voluntarily.

2. Certification

When you have completed the form, sign and print the name, title and date. For 7A and DUAL filers, the CHAR500 must be signed by both the president or another authorized officer and the chief financial officer or treasurer. These must be different individuals. EPTL filers have the option of a single signature if the certification is by a banking institution or a trustee of a trust. Clearly state the title of the representative (e.g. "President," "CEO", Treasurer," "CFO," "Bank Vice President" or "Trustee").

3. Annual Reporting Exemption

You may claim an exemption from the reporting and fee requirements if you meet the filing exemptions applicable to your organization. If claiming an exemption under one statute (7A and EPTL only filers) or both statutes (DUAL filers) that apply to your registration, complete only parts 1, 2, and 3, and submit the certified Char500. No fee, schedule, or additional attachments are required. Otherwise, file all required schedules and attachments and pay applicable fees.

Note: A 7A or DUAL filer with contributions over $25,000 that did not contract with a professional fund raiser may check the 7A filing exemption in Part 3 if it (i) received all or substantially all of its contributions from a single government agency to which it submitted an annual report similar to that required by Executive Law Article 7A, or (ii) it received an allocation from a federated fund, United Way or incorporated community appeal and contributions from all other sources did not exceed $25,000.

4. Schedules and Attachments

If you do not qualify for the reporting exemptions as described in Part 3, review the checklist of schedules and attachments required to complete your filing. If your organization qualified for and submitted an IRS

5. Fee

Your total fee is based on your registration category (7A, EPTL or DUAL). 7A or EPTL filers only pay the fee that applies to the statute under which they have registered unless they have claimed an exemption in Part 3. DUAL filers must pay both fees, unless they have claimed an exemption in Part 3. Consult the CHAR500 to calculate your fee or contact the NY Charities Bureau if you have additional questions.

When to Submit Your Filing

7A and DUAL filers: postmarked within 4 1/2 months after the organization's accounting period ends. For example, fiscal year end December 31 reports

are due by May 15th of the following year. EPTL filers: postmarked within 6 months after the organization's accounting period ends. An additional 180 day extension is automatically granted. Information regarding extensions is available at www.CharitiesNYS.com.

Where to Submit Your Filing

Payment must be made to the "Department of Law". Send the complete filing with payment to:

NYS Office of the Attorney General, Charities Bureau Registration Section, 28 Liberty Street, New York, NY 10005.

Penalties

The Attorney General may cancel the registration of or seek civil penalties from an organization that fails to comply with the filing requirements.

CHAR500 Instructions for Completing Your NY Annual Filing (Updated January 2020) |

Page 1 |

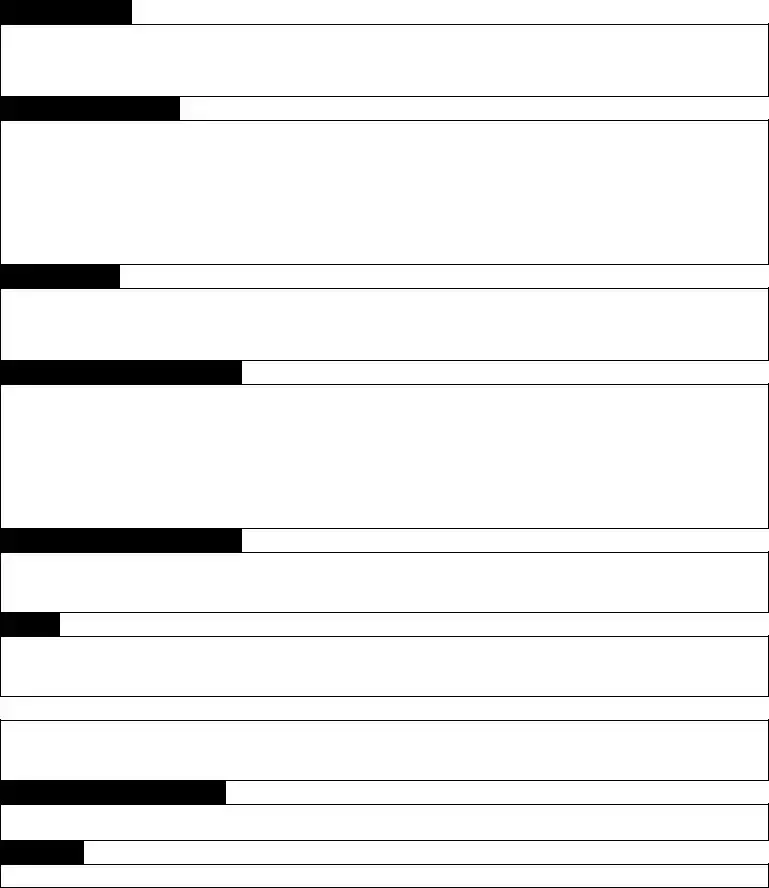

CHAR500

Schedule 4a: Professional Fund Raisers, Fund Raising Counsels, Commercial

2019

Open to Public

Inspection

If you checked the box in question 4a in Part 4 on the CHAR500 Annual Filing for Charitable Organizations, complete this schedule for EACH Professional Fund Raiser (PFR), Fund Raising Counsel (FRC) or Commercial

Definitions

A Professional Fund Raiser (PFR), in addition to other activities, conducts solicitation of contributions and/or handles the donations (Article 7A,

A Fund Raising Counsel (FRC) does not solicit or handle contributions but limits activities to advising or assisting a charitable organization to perform such functions for itself (Article 7A,

A Commercial

charitable organization (Article 7A,

Professional fund raising does not include activities by an organization's development staff, volunteers, or a grantwriter who has been hired solely to draft applications for funding from a government agency or tax exempt organization.

1. Organization Information

Name of Organization:

NY Registration Number:

- |

|

- |

|

|

|

2. Professional Fund Raiser, Fund Raising Counsel, Commercial

Fund Raising Professional type:

Professional Fund Raiser

Fund Raising Counsel

Commercial

Name of FRP:

Mailing Address:

City / State / Zip:

NY Registration Number:

- |

|

- |

|

|

|

Telephone:

3. Contract Information

Contract Start Date:

Contract End Date:

4. Description of Services

Services provided by FRP:

5. Description of Compensation

Compensation arrangement with FRP:

Amount Paid to FRP:

6. Commercial

Yes |

|

No |

If services were provided by a CCV, did the CCV provide the charitable organization with the interim or closing report(s) required by |

|

|||

|

Section 173(a) part 3 of the Executive Law Article 7A? |

||

|

|

|

CHAR500 Schedule 4a: Professional Fund Raisers, Fund Raising Counsels, Commercial |

Page 1 |

CHAR500

Schedule 4b: Government Grants www.CharitiesNYS.com

2019

Open to Public

Inspection

If you checked the box in question 4b in Part 4 , complete this schedule and list EACH government grant award by a domestic (federal, state or local) agency; interstate or intergovernmental agency (for example Port Authority of New York and New Jersey); and state or local authorities.

Use additional pages if necessary. Include this schedule with your certified CHAR500 NYS Annual Filing for Charitable Organizations.

1. Organization Information

Name of Organization:

NY Registration Number:

-

-

2. Government Grants

Name of Government Agency |

Amount of Grant |

|

|

1. |

1. |

|

|

2. |

2. |

|

|

3. |

3. |

|

|

4. |

4. |

|

|

5. |

5. |

|

|

6. |

6. |

|

|

7. |

7. |

|

|

8. |

8. |

|

|

9. |

9. |

|

|

10. |

10. |

|

|

11. |

11. |

|

|

12. |

12. |

|

|

13. |

13. |

|

|

14. |

14. |

|

|

15. |

15. |

|

|

Total Government Grants: |

Total: |

|

|

CHAR500 Schedule 4b: Government Grants (Updated January 2020) |

Page 1 |

Completing the CHAR500 form for New York State can be a daunting task, and many organizations make common mistakes that can lead to complications. One frequent error occurs when organizations fail to check the appropriate boxes for their filing type. For example, neglecting to indicate whether the filing is an initial, amended, or final submission can create confusion and delay processing. It is crucial to ensure that the correct status is marked to avoid unnecessary complications.

Another common oversight is the failure to provide complete and accurate contact information. Organizations often rush through this section, omitting critical details such as the mailing address, phone number, or email address. Incomplete contact information can hinder communication from the Charities Bureau, potentially leading to missed notifications or requests for additional documentation.

Many filers also miscalculate their fees. The fee structure is based on the organization’s registration category and net worth. Organizations may mistakenly assume they qualify for a lower fee without carefully reviewing their financial status. It is essential to accurately assess net worth and apply the correct fee to avoid penalties or delays in processing.

In addition, organizations sometimes overlook the necessity of including required schedules and attachments. If a professional fundraiser was used or if government grants were received, specific schedules must be completed and submitted with the CHAR500. Failing to include these documents can result in rejection of the filing.

Certification errors represent another significant pitfall. The CHAR500 must be certified by two individuals: the president or an authorized officer and the chief financial officer or treasurer. If the same person signs both places, this violates the certification requirement. Ensuring that different individuals sign and that all required titles are included is vital for compliance.

Moreover, organizations frequently misinterpret the exemption criteria. Claiming an exemption when the organization does not meet the specific requirements can lead to complications. It is crucial to understand the criteria for exemptions under 7A and EPTL and to ensure that all necessary documentation is provided if exemptions are not applicable.

Another mistake involves the use of outdated forms. Organizations sometimes download older versions of the CHAR500, which may not reflect the most current regulations or requirements. Always ensure that the latest version of the form is being used to avoid unnecessary issues.

Lastly, many organizations neglect to review their filings thoroughly before submission. Typos, incorrect figures, or missing information can lead to significant delays. A careful review of the entire form and all attachments can prevent these errors and ensure a smoother filing process.

The CHAR500 form is an annual filing required by the New York State Office of the Attorney General for charitable organizations. It serves to report financial information and ensure compliance with state regulations. Organizations must submit this form along with any necessary fees and attachments.

Any charitable organization registered in New York State must file the CHAR500. This includes organizations registered under the 7A, EPTL, or DUAL categories. If your organization is exempt, you may still choose to file voluntarily.

Filing deadlines vary based on your organization’s registration category. For 7A and DUAL filers, the CHAR500 must be postmarked within 4.5 months after the fiscal year ends. For EPTL filers, the deadline is 6 months after the fiscal year ends, with an automatic 180-day extension available.

If your organization qualifies for a filing exemption, you only need to complete Parts 1, 2, and 3 of the CHAR500 and submit the certified form. No fees or additional attachments are required. Ensure you meet the criteria for the exemption to avoid penalties.

NET WORTH is calculated based on specific IRS forms. For instance, it can be found on IRS Form 990, Part I, line 22, or on IRS Form 990-EZ, Part I, line 21. If your organization files IRS Form 990-PF, calculate the difference between total assets and total liabilities to find your NET WORTH.

Fees depend on your organization’s registration category and whether you claim any exemptions. For 7A and EPTL filers, fees range from $0 to $1,500 based on NET WORTH. DUAL filers must pay both applicable fees unless exempt.

Submit the completed CHAR500 form, along with any schedules, attachments, and payment, to the following address: NYS Office of the Attorney General, Charities Bureau Registration Section, 28 Liberty Street, New York, NY 10005.

Failure to file the CHAR500 can result in penalties, including the cancellation of your organization’s registration. The Attorney General may seek civil penalties for non-compliance. It's crucial to adhere to filing requirements to maintain your organization’s status.

This is incorrect. The CHAR500 is required for all charitable organizations, regardless of size. Even small organizations must file if they meet certain criteria.

While some organizations may qualify for exemptions, they still must submit the CHAR500 form to confirm their exempt status. Failure to do so can lead to penalties.

Both the president or authorized officer and the chief financial officer or treasurer must sign the form. This requirement ensures accountability and accuracy in reporting.

Different types of organizations have varying deadlines. For example, 7A and DUAL filers must submit their filings within 4.5 months after their fiscal year ends, while EPTL filers have 6 months.

The NY Charities Bureau does not accept the IRS 990-N e-postcard for filing. Organizations must submit the IRS Form 990-EZ instead, as it contains more detailed financial information.

The CHAR500 must be filed annually. Organizations are required to file every year to maintain compliance with New York state regulations.

Even organizations that do not actively solicit contributions may still be required to file the CHAR500. If they hold assets or conduct charitable activities in New York, filing is necessary.

Mcs-150 Update - The document must be completed accurately to ensure compliance with transportation regulations.

New York 1481 - Returning the completed form ensures it reaches the correct department for approval.

Tr2 Form - Submitting the TR2 form correctly helps to ensure project compliance with regulations.

Filling out the CHAR500 form for New York State is an essential task for charitable organizations. Here are some key takeaways to keep in mind:

Completing the Char500 NYS form is an essential step for charitable organizations operating in New York. This process requires careful attention to detail to ensure compliance with state regulations. The following steps outline how to accurately fill out the form, which must be submitted along with the appropriate fees and any necessary attachments.

After submitting the form, it is crucial to keep a copy for your records. Stay informed about any communications from the Charities Bureau, as they may require additional information or clarification regarding your submission.